When Every Clock Counts Down to the Same Day: The Endgame Structure from Tokyo 1945 to Tehran 2026

Why this war ends with silence, not a ceasefire — and what allocators should watch for

Key Takeaways

This war will not end with a surrender ceremony. It will end with silence. Attack frequency drops. Statements disappear. The Strait gradually reopens. When every participant’s window closes simultaneously, the absence of action becomes the ceasefire.

The structural parallels between Japan’s military establishment in 1945 and the IRGC in 2026 (independent economies, independent command chains, ideological self-legitimization) dictate the shape of the exit: not a signed document, but a progressive zeroing-out of offensive capability.

Two critical differences accelerate the exit but complicate the aftermath. Precision strikes replaced total destruction, meaning the IRGC’s weapons are gone but the country is intact. And Iran’s land borders and proxy networks, unlike Japan’s island geography, allow residual low-intensity harassment even after the homeland military capability is eliminated.

Multiple timelines converge on late March. Design or coincidence, the result is the same.

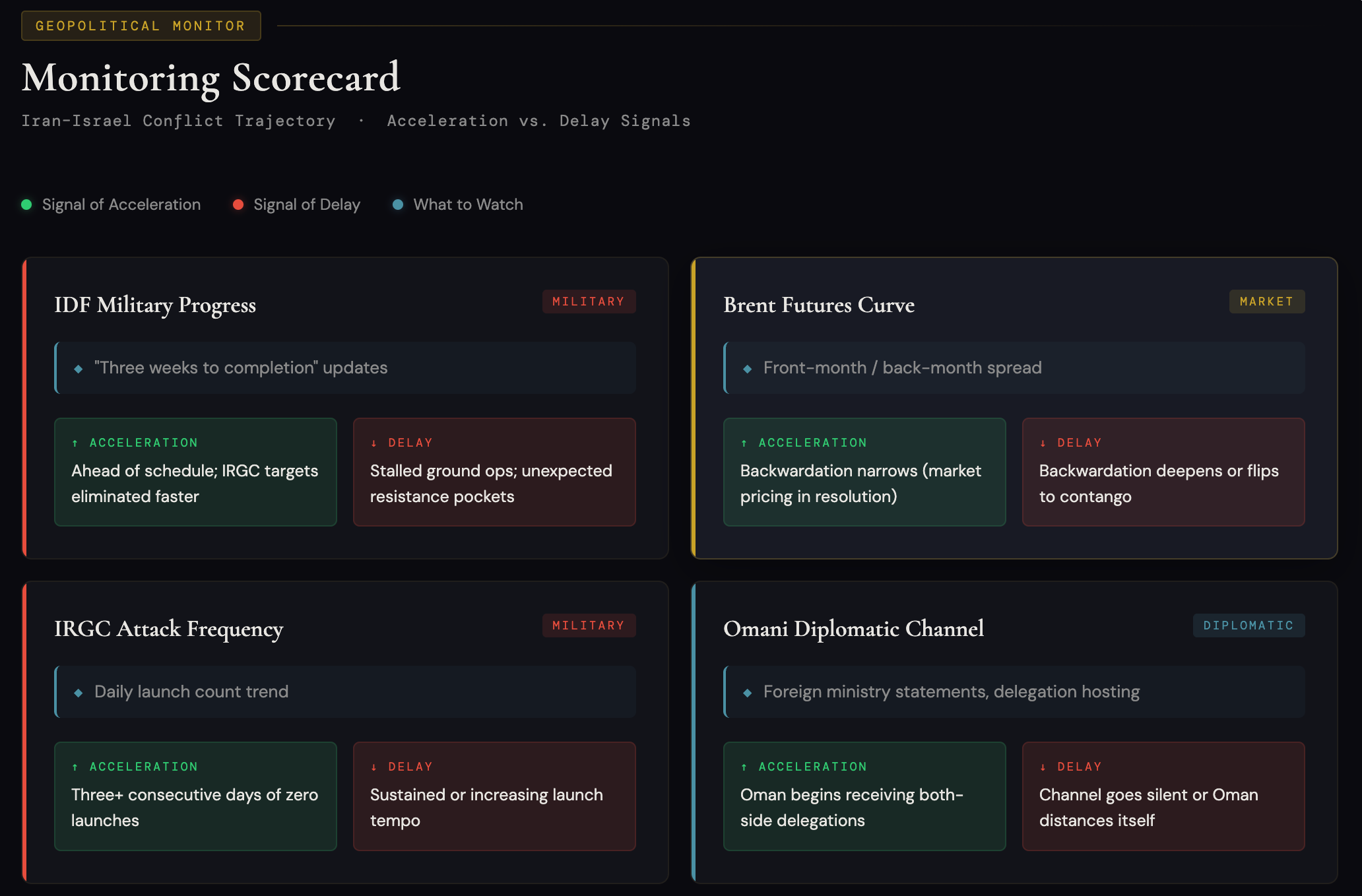

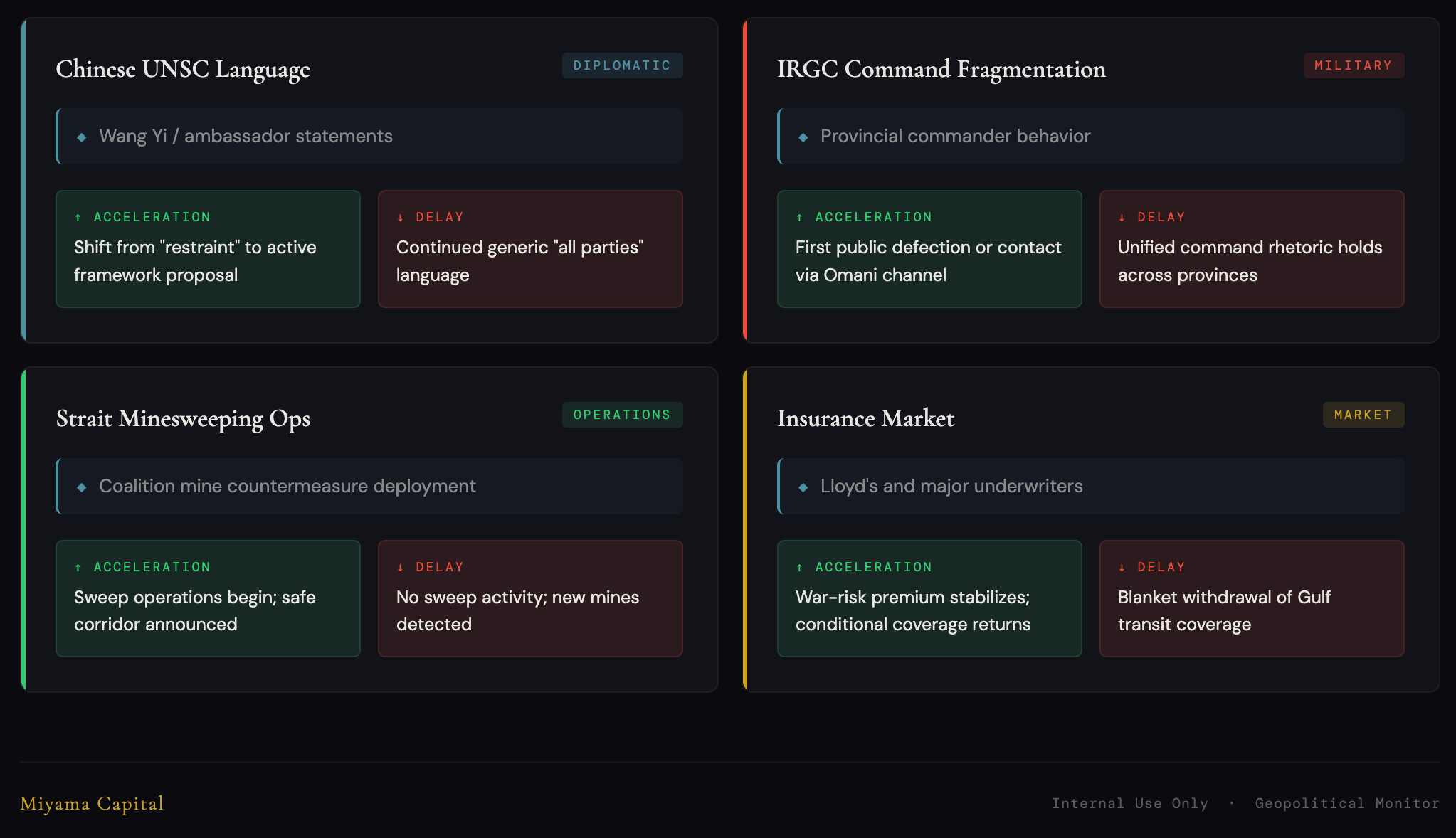

Watch List: IDF progress updates on “three weeks to completion,” Brent front-month/back-month spread (backwardation persistence), Omani diplomatic channel activity, Chinese language shifts at the UNSC, IRGC command chain fragmentation velocity, Strait minesweeping operation launch timing. Assumption invalidation trigger: a successful IRGC attack on Gulf state oil infrastructure causing multi-month production disruption (not short-term harassment) would extend the exit timeline, potentially push oil above $130, and require full scenario recalibration.

I. The Echo of the Kyūjō Incident

On the night of August 14, 1945, a group of junior officers in the Japanese War Ministry launched a coup. Their objective was specific: intercept the Emperor’s pre-recorded surrender announcement, a recording known as the Jewel Voice Broadcast, before it could be aired to the nation the following day. The plotters searched the Imperial Palace room by room. They failed to find the recording. At noon the next day, radios across Japan carried the Emperor’s voice for the first time in history.

The war was over. But the attempted coup itself revealed something more important than the military outcome. Losing does not mean willing to stop.

Eighty-one years later. Tehran, March 2026.

President Pezeshkian attempted a public apology and signaled reconciliation to the international community. Within days, he was forced to reverse course, issuing a Telegram statement endorsing the new Supreme Leader Mojtaba Khamenei, praising Iran’s “resilience and unity.” A president wrapping his own submission in diplomatic language is structurally identical to the palace aides physically hiding the surrender recording during the Kyūjō Incident. The pragmatists know it is time to stop. But a force within the system refuses to accept reality.

In the previous article, I analyzed why all participants are being pushed toward convergence. This article asks the next question: What does the exit look like? How fast? Then what?

II. The Structural Parallel Between the Imperial Military and the IRGC

Three layers of institutional similarity connect Japan’s military establishment in 1945 and Iran’s Islamic Revolutionary Guard Corps in 2026.

Start with the economics. The Japanese military controlled Manchuria’s industrial resources, munitions production, and vast overseas assets. It functioned as an economic entity outside civilian cabinet oversight. The IRGC’s economic empire is larger. It spans oil, construction, telecommunications, and finance, accounting for an estimated 20 to 30 percent of Iran’s GDP. This is not “a military doing business.” It is a quasi-state with its own profit motive. When you ask an organization to surrender, you are not just asking it to lay down weapons. You are asking it to abandon an entire economic ecosystem.

Then there is the command structure. The Japanese military’s supreme command authority reported directly to the Emperor. The civilian cabinet had no jurisdiction. The IRGC reports directly to the Supreme Leader. The president has no jurisdiction. Both are a state within the state, operating their own intelligence apparatus, their own foreign relationships, their own strategic logic. Pezeshkian cannot control the IRGC any more than Prime Minister Koiso could control the military after Tojo.

The deepest layer is ideological. The military defined itself as the guardian of the kokutai, the national polity. The survival of the Emperor system depended on the survival of the military. The IRGC defines itself as the guardian of the revolution. The survival of the Islamic Republic depends on the survival of the IRGC. This is what makes surrender existentially different from losing a war. Not “we lost.” “We cease to exist.”

Predictably, after Mojtaba took over, the IRGC’s rhetoric skipped “let us negotiate terms” and went straight to “continue the fight.” When Foreign Minister Araghchi refused a ceasefire on Meet the Press, it was not because he believed Iran could win. Within the IRGC’s framework, accepting a ceasefire means accepting the IRGC’s dissolution. The same logic drove the Kyūjō plotters: accepting surrender meant accepting the end of the kokutai.

III. Two Critical Differences: Faster Exit, Messier Aftermath

I will address the two fundamental differences proactively.

Difference one: precision strikes replaced total destruction.

The logic of 1945 was to destroy everything, then wait for the other side to accept reality amid the rubble. Hiroshima, Nagasaki, the firebombing of Tokyo. Destruction was area-wide and irreversible. The logic of 2026 is categorically different. The U.S.-Israeli coalition destroyed 90% of the IRGC’s missile capability, 43 naval vessels, and 80% of air defense systems within ten days, while deliberately avoiding civilian infrastructure and oil production facilities. U.S. Energy Secretary Chris Wright stated explicitly that the U.S. would not target energy infrastructure.

The U.S.-Israeli coalition systematically dismantled the IRGC’s military capability, but the country has not been destroyed. The foundation for postwar reconstruction remains intact. This distinction has an enormous impact on exit speed. Japan needed nearly a month to “digest” the reality of annihilation, from Hiroshima (August 6) through the Kyūjō Incident (August 14) to the signing aboard the USS Missouri (September 2). Iran’s IRGC does not need to digest national destruction. It needs to digest a sharper fact: my weapons are gone, but my country is still here, and my country’s future does not require me.

Difference two: island nation versus continental depth.

Japan in 1945 was an island nation. Once the naval blockade was in place, there was no escape route. Iran is different. It shares land borders with Iraq, Afghanistan, Pakistan, and Turkmenistan. It maintains proxy networks extending into Lebanon, Syria, and Yemen. Even if the IRGC is broken on home soil, remnant forces can disperse, infiltrate neighboring states, and sustain low-intensity harassment.

This is my biggest reservation about a “clean exit.” Israel can complete the destruction of the IRGC’s homeland military capability within three to four weeks. The IDF itself stated it needs “three more weeks.” But eliminating homeland capability does not mean eliminating the proxy network. Mines already laid in the Strait do not disappear because IRGC headquarters was destroyed. The military exit will be fast. The political cleanup will be slow.

For allocators, the practical implication is this: oil prices will likely drop quickly once direction is confirmed (markets trade expectations), but the physical restoration of the Strait, including minesweeping, safety verification, insurance reinstatement, and shipowners’ willingness to transit, could drag into mid-April or even May. The front-month/back-month spread will tell you what the market thinks. As of this writing, Brent hit an intraday high of $119.50 before pulling back sharply to the low $90s, largely on G7 discussions of a coordinated strategic petroleum reserve release. Backwardation remains pronounced: front month around $90-98, the October contract around $76-80 (source: Bloomberg, as of 2026/03/09). The pullback itself confirms the thesis. The market is saying: direction confirmed, timing uncertain. The spike was panic; the retreat is the market pricing in that the Strait will eventually reopen.

The most common counterargument is that the IRGC’s proxy network could drag the conflict into prolonged harassment. This risk is real, and the second difference already identified the problem of continental depth and proxy infrastructure. But it changes the complexity of the postwar order, not the direction of the war’s exit. Proxies can extend harassment. They cannot restore the IRGC’s homeland missile, naval, and air defense capability. Harassment and warfighting capability are categorically different.

IV. Engineered Deadline, or Coincidental Convergence?

Count backward from late March.

Based on current timelines, the Trump-Xi summit is expected on March 31. That is four to five weeks from the start of hostilities on February 28. The IDF stated on day ten that it needs “three more weeks to complete military objectives,” pointing to March 29-30. The White House public framing is “four to six weeks.” Every timeline converges on the same window.

This could be the product of deliberate design: war planners working backward from the endgame, selecting a start date that allows the military phase to conclude before the summit. It could also be the coincidental intersection of multiple constraints: military readiness achieved, intelligence confirmation complete, Iran’s nuclear program approaching criticality, the regime at its most fragile following January protests, with the summit date as a bonus rather than a primary driver.

Regardless of which explanation holds, the result is the same. Late March becomes a shared constraint for every participant.

Trump needs to bring results to Beijing. Xi needs a deal before oil prices inflict lasting damage on the Chinese economy: China imports over 70% of its oil, and even with Brent pulling back from $119 to the low $90s, the price is still 30%+ above prewar levels. At peak, the additional import cost reached roughly $15 billion per month. The pullback buys time but does not remove the pressure, especially for an economy already in deflation. Israel needs to complete its objectives before international pressure reaches the breaking point. Iran’s pragmatists need to reach the negotiating table while the IRGC still has some residual leverage to offer. Gulf states need to resume exports before storage capacity runs out. Kuwait and Iraq are already cutting production. This is happening, not speculation.

All five timelines point to the same window. As of this writing, that window is less than three weeks away. If the summit proceeds as scheduled, it is not just a diplomatic event. It is where those five pressure lines intersect. But the war itself has injected new uncertainty into the summit’s timing and format. Nothing has been canceled, but nothing is locked either.

More notable is the pattern of timing gaps between negotiations and attacks. On February 6, indirect talks via Oman. On February 28, full-scale war. Iran’s Supreme National Security Council (SNSC) characterized this as being “attacked again during negotiations.” Looking back over the past year, a pattern of overlapping diplomatic and military timelines has emerged three times: the Twelve-Day War launched in June 2025 while nuclear negotiations were underway, nuclear facilities struck on June 22, 2025 during a ceasefire, and full-scale war on February 28, 2026 following the Omani channel talks. In each instance, diplomatic processes ran in parallel with attack preparations.

Whether this pattern reflects coordination or coincidence, the effect on Iran’s trust calculus is the same. This is what Araghchi means when he insists on “a permanent end to the war” rather than a ceasefire. He is not setting terms. He is expressing the fundamental distrust that builds after being hit by the same pattern three times. The SNSC framed the latest episode as being “attacked while negotiating.” Whether or not one accepts that characterization, the pattern itself shapes Iran’s negotiating posture. The cost of rebuilding trust after the third iteration is not something a single agreement can cover.

V. The Pragmatists’ Survival Game

The question facing Pezeshkian and Araghchi is not “whether to surrender.”

The question is “how to survive after the IRGC weakens.”

According to Carnegie Endowment senior fellow Karim Sadjadpour in a March 2026 CNN interview, Mojtaba Khamenei is currently injured, in hiding, and facing public chants calling for his death. Sadjadpour cited someone who has known Mojtaba for years: “He doesn’t care about ruling. He cares about staying alive.” Wartime information is inherently noisy, and these details will need continuous verification. But if this assessment holds even directionally, Mojtaba is at most a transitional figure whose political legitimacy could reach zero within weeks, faster than the IRGC’s economic runway.

The pragmatists’ calculus is therefore extremely delicate.

Openly confront the IRGC? Physical safety is directly at risk. An IRGC that has lost its external battlefield will only become less tolerant of internal dissent. Pezeshkian’s decision to publicly endorse Mojtaba is almost certainly a survival strategy: do not collide head-on with a collapsing organization; wait for it to fall on its own.

But waiting has costs. Every additional day, the pragmatists’ negotiating leverage erodes. Right now, they can still offer something: “I can help you reopen the Strait,” because minesweeping requires Iranian cooperation on mine locations and restraint of residual coastal forces. Three to four weeks from now, if Israel has fully cleared the IRGC’s coastal defenses, what the pragmatists can offer becomes far less valuable.

This is a two-sided squeeze. Move too early, get liquidated by IRGC remnants. Move too late, leverage goes to zero. Their optimal window is roughly when IRGC military capability approaches zero but political fragmentation is not yet complete. By my estimate, that window falls somewhere between mid-March and late March.

There is one underestimated variable here: the economic incentive. Global oil prices remain elevated well above prewar levels, even after the pullback from $119. If Iran can resume oil exports postwar, revenue would be significantly higher than before the conflict. The pragmatists have a very concrete argument they can make to the IRGC’s economic wing: “Stop the war now, resume exports, and oil revenue could hit historic highs.” Revenue projections at current prices may carry more weight with the IRGC’s economic wing than revolutionary rhetoric.

VI. There Will Be No USS Missouri Signing

September 2, 1945. Tokyo Bay. On the deck of the USS Missouri, Japanese representatives signed the instrument of surrender.

This scene will not be replicated in 2026.

Iran’s institutional structure does not permit anyone to publicly sign a “surrender.” The Supreme Leader’s theological authority, the IRGC’s revolutionary narrative, Shia resistance theology: all of these reject any form of public capitulation. But more importantly, the U.S. does not need a signing ceremony either. Defense Secretary Hegseth said it clearly on 60 Minutes: “We’ll know when they no longer have the ability to fight.” Not waiting for Iran to say it surrenders. Waiting for the IRGC to be unable to continue.

So the exit will take the form of progressive silence.

Attack frequency declines. Statements become less frequent. Threats stop. Strait harassment goes from daily to weekly to sporadic. Then one day, the Omani channel produces a “framework,” worded vaguely enough for everyone to accept: “Both sides agree to pursue lasting peace through diplomatic channels.” Nobody admits this is a surrender. Because it is not. It is a silent transition after military capability reaches zero.

Trump told the Times of Israel, “I’ll decide when it ends.” Asked whether Israel would continue strikes after the U.S. stops, he said: “I don’t think that will be necessary.” This implies a coordinated exit tempo between the U.S. and Israel: synchronized ceasefire, not independent action.

For allocators, the signal to watch is silence, not a ceasefire announcement. When the IRGC goes three consecutive days without launching anything; when Araghchi’s language shifts from “continue the fight” to “lasting peace”; when Oman’s foreign ministry starts receiving delegations from both sides: the exit is underway. You do not need a voice to announce the end.

VII. Accepting Reality Is a Curve, Not a Moment

Japan needed eight days from Hiroshima to the Jewel Voice Broadcast.

But those eight days were not “suddenly coming to one’s senses on a particular day.” They were a sequence of micro-collapses. The Soviet entry into the war shattered the last diplomatic fantasy. Nagasaki eliminated the hope that Hiroshima was an isolated event. The failure of the military’s counter-coup made the Emperor’s decision irreversible. Each event pushed the “accepting reality” curve up one notch.

Where is Iran on this curve?

My assessment: past the midpoint.

The first shock was February 28, when Khamenei and roughly thirty senior officials were eliminated simultaneously. This was not merely a military strike. It was a signal to the entire system: your top layer no longer exists. The second was the rapid depletion of IRGC missiles, from over 3,000 at the start of hostilities to near zero within ten days. The third was the continued attacks on Gulf states that the IRGC could not prevent: the Bahrain desalination plant hit, the Saudi Shaybah oil field attack intercepted. The IRGC can still harass, but it can no longer defend. The fourth was Mojtaba’s weakness: reportedly injured, in hiding, facing public death chants. If even half of the reporting is accurate, a Supreme Leader who cannot protect himself cannot sustain organizational loyalty.

What is still missing? The collective-action tipping point among provincial commanders.

IRGC provincial commanders now face a classic collective action problem. If everyone stays loyal, the system has a slim chance. If someone defects first, the first mover survives best. But who moves first? Information is opaque. Communications are severed. Headquarters no longer exists. Every commander is guessing what the others will do. Once the first provincial commander publicly refuses allegiance to Mojtaba, the cascade will be fast, because everyone is waiting for that signal.

This is the mirror image of the Kyūjō Incident. The failed coup in 1945 was the tipping signal: “even the military itself cannot prevent surrender.” The 2026 version may be a provincial IRGC commander ceasing attacks or making contact through the Omani channel.

VIII. China’s Leverage Is Decaying: Every Day It Gets Thinner

China is the most urgent but least visibly urgent participant in this conflict.

The numbers are brutal. China imports over 70% of its oil. Brent surged from a prewar $69 to an intraday high of $119.50 before pulling back to the low $90s. Even at current levels, the additional daily import cost runs roughly $250 million (based on approximately 11 million barrels per day of imports and a price increase of approximately $25 per barrel from prewar). At peak, the daily burn rate was nearly double that. For an economy already struggling with deflation, with CPI near zero, real estate confidence unrecovered, and exports under tariff pressure, any sustained oil premium is a bad combination. Cost-push inflation layered on top of demand weakness. Raise rates and you kill real estate. Cut rates and the renminbi depreciates, making imports even more expensive. The pullback from $119 to $90 provides relief, not resolution.

But what matters most for allocators is that China’s leverage is decaying over time. The pain itself is secondary.

Right now, China’s value lies in its ability to offer Iran a “security guarantee that does not come from the United States.” Iran does not trust the U.S. (the JCPOA lesson), does not trust Israel, and has limited trust in Russia. China is Iran’s largest oil customer. It has economic leverage. It holds a UN Security Council veto. If the final deal requires a guarantor, China is the role most likely to be accepted by Iran.

But this role has an expiration date.

Three weeks from now, if Israel completes its “three-week” military objectives and the IRGC’s coastal defenses are cleared, Iran’s “we won’t reopen the Strait” leverage is shrinking. China’s security guarantee as “the key to reopening the Strait” becomes less necessary. Six weeks from now, if the IRGC is fully at zero, Iran has no bargaining chips left. The only path is accepting whatever terms the U.S. offers. China’s guarantee downgrades from must-have to nice-to-have.

Xi almost certainly understands this. Wang Yi’s March 8 statement was not randomly timed. It came after Mojtaba’s ascension and oil breaking $100. “A war in which nobody benefits” is laying the groundwork for intervention.

This is the critical node of cross-asset transmission. The geopolitical event transmits through China’s policy choices into oil prices, the renminbi, and Asian credit. If Xi obtains tariff relief at the summit in exchange for cooperation on the Iran endgame, the transmission path is: China pressures Iran → exit framework emerges → oil price expectations decline → renminbi pressure eases → Asian credit spreads tighten. Conversely, if the summit produces no consensus: oil stays above $100 → Chinese recession risk rises → renminbi weakens → Asian credit spreads widen → emerging market dollar-denominated debt comes under pressure.

China’s window to act is between now and March 31. After that, whether it acts or not, the value of its intervention declines sharply.

IX. Implications for Asset Allocators

I will not tell you what to buy or sell. But I will analyze the transmission logic so you can apply your own framework.

Energy. Brent has pulled back sharply from its intraday high of $119.50 to the low $90s, largely on G7 discussions of a coordinated strategic petroleum reserve release. The most important signal now is the futures curve’s backwardation structure. Front month around $90-98, back months in the upper $70s: the market believes the supply squeeze is temporary and that the Strait will eventually reopen. If backwardation starts flattening or flips to contango (back months more expensive than front), the market is saying “this time is different.” As of this writing, that has not happened. Political intervention can suppress short-term panic, but it does not solve the fundamental supply problem. The fundamental problem is when the Strait resumes transit, and that depends on minesweeping, coastal defense clearance, insurance reinstatement: a process that could take six to ten weeks.

Inflation and central bank path. Oil above $100 sustained for more than four weeks would likely push headline CPI from the 2.5% range toward 3.0-3.5%. Core CPI absorption is slower but has already begun: transportation costs feed into food prices feed into service-sector costs. The Fed’s most probable response is a hold, meaning “look through” the geopolitical supply shock. But rate-cut expectations effectively disappear. If oil stays above $100 for more than eight weeks, the market will begin pricing in a tail-risk path of “forced to consider rate hikes due to geopolitical inflation.” This is extremely rare in the Fed’s historical behavior. During the 2022 Russia-Ukraine war, the Fed chose to hike, but primarily in response to preexisting broad inflationary pressure, not a pure geopolitical supply shock. Whether this scenario triggers a similar response depends on whether core CPI follows.

Currencies. The dollar continues to strengthen on safe-haven demand plus interest rate differentials. DXY is likely in the 103-105 range. Oil-importing currencies are under pressure, particularly the Indian rupee, Korean won, and renminbi. For allocators with Asian exposure, hedging costs are rising.

Asian credit. Oil spike plus dollar strength equals a double hit. South Korea has already triggered circuit breakers. India’s current account is deteriorating. Japan’s import costs are surging. If this state persists into mid-April, emerging market dollar bond spreads will begin reflecting recession risk, not merely a geopolitical risk premium.

⚠️ The transmission paths above describe conditional scenario logic (”if oil stays above $100 for X weeks”), not predictions. The duration of elevated oil prices depends on exit speed, and exit speed is being accelerated by every structural force analyzed in this article.

X. Conclusion

Every pressure line points to the same window.

On the military front, Israel says three weeks. On the economic front, oil prices remain elevated well above prewar levels, pushing every side’s tolerance toward its limit. On the political front, if the summit proceeds as scheduled, it is the convergence point of five timelines. On the institutional front, Mojtaba’s authority is declining daily. The collective-action tipping point among provincial commanders could arrive at any moment.

This war will not end with a signing ceremony.

It will end the way Tokyo ended in 1945. Forces within the system try to prevent reality from arriving. Then at some point, the weight of reality exceeds the capacity for resistance, and silence begins to spread. Attack frequency drops. Statements disappear. The Strait slowly reopens. Nobody announces surrender. Because structurally, this is not a surrender. It is a silent transition after military capability reaches zero.

You do not need a voice to announce the end. You just need enough silence.

Monitoring Scorecard

Scenario Analysis

⚠️ The probabilities below are illustrative, intended to show the relative weight of each path within the framework. They should not be used as a basis for trading decisions.

Base Case (estimated probability ~55-60%)

Assumptions: Israel completes primary military objectives within three to four weeks. IRGC homeland offensive capability approaches zero. The Omani or Chinese channel produces some form of framework consensus. Oil prices begin retreating once directional clarity emerges.

Monitoring indicators: Sustained decline in IRGC attack frequency. Omani foreign ministry statement language. Changes in Brent front-month/back-month spread.

Positioning implications: Prepare for short-term energy volatility, but do not adjust long-term allocation out of panic. Monitor “silence signals” as the basis for directional shifts.

Risk Case (estimated probability ~25-30%)

Assumptions: IRGC Strait harassment proves more persistent than expected. Mines, fast boats, and unmanned surface vessels maintain an unsafe Strait environment for more than six weeks. Minesweeping progress is delayed. The insurance market continues to withdraw coverage. Oil prices remain in the $100-130 range past mid-April.

Monitoring indicators: Success rate of Strait transit attempts. Minesweeping operation launch timing and progress. Lloyd’s and major insurers’ underwriting stance.

Positioning implications: Evaluate whether the cost of hedging energy exposure is justified. Assess whether currency risk on Asian credit positions needs to be reduced.

Tail Case (estimated probability ~10-15%)

Assumptions: Conflict escalates unexpectedly. IRGC remnant forces succeed in causing multi-month disruption to major Gulf state oil facilities, or the conflict spreads to new participants (e.g., residual Hezbollah forces opening a second front in Lebanon). Oil breaks above $130 and backwardation disappears or flips to contango.

Monitoring indicators: Substantive damage reports on Gulf state oil facilities. Structural breaks in the futures curve. Signs of third-country military involvement.

Positioning implications: This is the trigger for reassessing the entire geopolitical risk framework. A full recalibration, not an incremental adjustment.

Disclaimer

This article reflects my personal investment philosophy. It is not investment advice. Make your own informed decisions.

Miyama Capital manages proprietary capital only and does not solicit external investors.

This memo represents the author’s personal views on macroeconomic conditions, interest rate environments, and asset allocation as of the date of writing. It does not constitute a solicitation, recommendation, or guarantee regarding the purchase or sale of any security, fund, bond, or other financial instrument. Investing involves risk; bond prices, interest rates, foreign exchange rates, and economic/policy conditions may materially affect asset values. Scenarios and instruments discussed may become inapplicable as market conditions change. Readers who make investment decisions based on this memo do so at their own risk, and the author accepts no liability for any gains or losses arising from the use or citation of this material.

Kuan H. Wang Founder & CIO, Miyama Capital