Taiwan’s Forced Expansion: A Small-Open-Economy Case Study in Financial Repression

Why CPI stability and currency dilution can both be true at once, and what that means for an allocator’s balance sheet.

Miyama Capital | Investment Memo | May 2026

The Gap

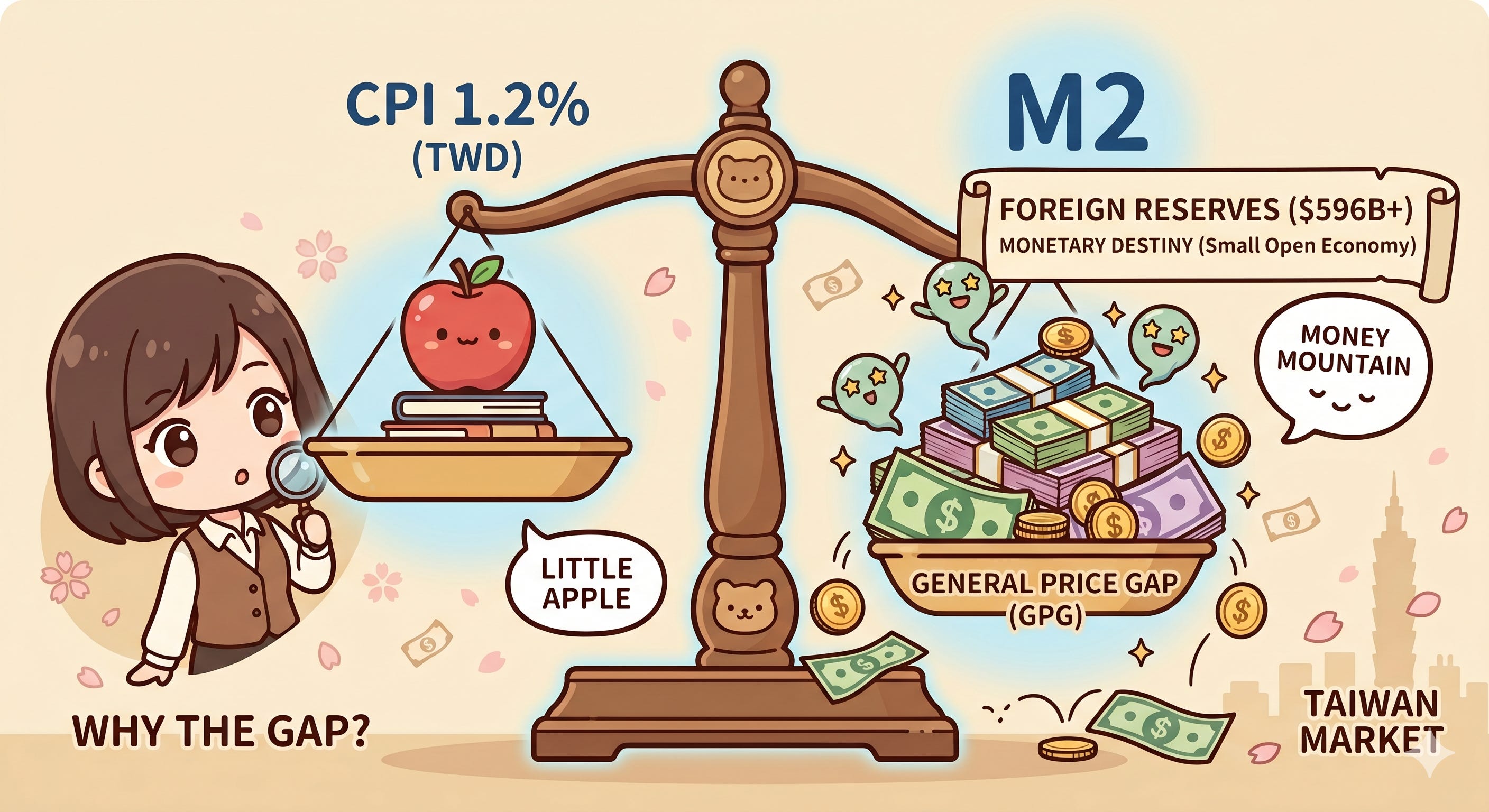

Taiwan’s CPI rose 1.23% year-over-year in Q1 2026. The central bank reports M2 of NT$68.45 trillion (approximately US$2.1 trillion at end-April 2026 spot) as of February 2026, with year-over-year growth of 5.38%. Both numbers fall within official targets. By any conventional reading, this is a successful price-stability regime.

Now widen the lens. Between 2010 and 2026, Taiwan’s M2 expanded from roughly NT$30 trillion to nearly NT$70 trillion. That is a 2.2x increase in fifteen years. Real GDP did not double over the same period. The gap between monetary expansion and real output is the structural artifact this memo is about.

My read is that the gap is not measurement error. It is the predictable output of a specific policy architecture operating under specific external constraints. Once the architecture is laid out, the gap stops looking like a Taiwan-specific anomaly and starts looking like a small-open-economy instance of a far more general phenomenon: financial repression as the equilibrium response to high sovereign and quasi-sovereign debt loads.

This memo treats Taiwan as a case study. The mechanics travel.

The Transmission Chain

The chain runs as follows:

Export surplus → USD inflow → FX conversion pressure on the local currency → Central bank intervention to absorb USD and prevent excessive appreciation → New TWD released into the banking system → Sterilization via NCD issuance → Residual liquidity leaks into asset markets

The trigger end of the chain in Taiwan’s current cycle is the AI and semiconductor supply chain export surge. Per the Central Bank of the Republic of China (Taiwan)’s December 2025 board meeting reference materials, total exports rose 34.1% year-over-year in the first eleven months of 2025. Electronics and ICT products reached 73.7% of total exports. Exports to the United States hit 30.4% of the total, surpassing the 26.8% share going to mainland China for the first time. The CBC’s own 2025 GDP forecast came in at 7.31%, with twenty-institution consensus at 6.7%.

An export surge of that magnitude generates an equivalent magnitude of USD-to-TWD conversion pressure. The CBC then faces a constrained choice. The choice is not whether to intervene. It is which cost to absorb.

Letting TWD appreciate freely sacrifices the price competitiveness of traditional industries and export-oriented SMEs, with downstream employment consequences. Holding TWD relatively weak requires absorbing the local-currency liquidity released by USD purchases, plus accepting whatever asset-market spillovers result from incomplete sterilization.

Taiwan, like every small open economy that has built its growth model on exports, has structurally chosen the second cost. This is a national-level revealed preference embedded in the export-led growth model itself, not a CBC decision in any narrow sense.

Why the Central Bank Has No Choice

The CBC’s February 2026 Monetary Policy Framework Operational Strategy Review is unusually candid on this point. The report uses the term small open economy explicitly and cites IMF and BIS research on why the exchange-rate channel dominates the interest-rate channel in such economies. It calculates sterilization coefficients for Taiwan, Korea, Singapore, and Hong Kong, the empirical estimate of what fraction of FX-intervention-released local liquidity is reabsorbed by the central bank’s sterilization tools.

The CBC’s December 2025 reference materials directly engage with an article in The Economist that described the architecture as follows: CBC keeps TWD structurally weak to support export competitiveness, intervenes in FX swap markets to reduce the currency mismatch risk facing Taiwan’s life insurance sector, and thereby enables the channeling of roughly $960 billion in household savings, via $700 billion in life insurer overseas assets, into U.S. Treasuries. This forms a “household savings → life insurers → UST” pipeline.

The CBC’s response is not denial. It is point-by-point justification: the historical reasons for life insurer currency mismatch, the role of sterilization tools in “appropriately managing banking system liquidity,” and the observation that TWD has appreciated roughly 11.8% from its 2022 low of 34.896 to 31.202 in December 2025, therefore (in the CBC’s framing) not “deliberately suppressed.”

What the CBC is not contesting is the giveaway. The pipeline’s existence goes unchallenged. So does the structural capture of household savings into a foreign sovereign bond holding. The CBC contests only the characterization of intent. The architecture is acknowledged because it is acknowledged on the record.

The primary sterilization instrument is the Negotiable Certificate of Deposit (NCD). After USD purchases release TWD into the banking system, the CBC issues NCDs; banks use excess reserves to “buy” them; local liquidity is locked back onto the central bank’s liability side. The NCD outstanding balance stood at roughly NT$9 trillion entering 2026. That number, by itself, is a record of cumulative intervention pressure.

Sterilization is never 100%. Academic estimates place Taiwan’s historical sterilization coefficient at roughly 0.85 to 0.95. The reason is structural: when NCD outstanding reaches NT$9 trillion, further sterilization compresses bank lending capacity and inflates central bank interest expense. The 85–95% range is the institutional ceiling, rather than a policy choice.

That residual 5–15%, compounded over fifteen years of intervention, is the mechanical source of the M2-to-real-GDP gap. The key variable is the sterilization ceiling. It sits below 1, and the leak is structural.

I read this as the precise meaning of forced actor. The CBC is not unwilling to act differently. It is unable to.

The CBC report contains one technical detail that matters. The report states that “for many years, Taiwan’s M2 growth rate has approximately equaled real GDP growth plus CPI growth,” and cites this relationship as evidence that M2 expansion is sufficient to support economic activity while preserving price stability. The relationship is arithmetically correct. It also presupposes that the relevant “price” is CPI. Once housing, land, and equity-market repricing are folded into a broader definition of price, the equation develops a residual, and that residual is precisely the share of M2 expansion that lands in asset categories CPI does not capture.

My working model is simple. Taiwan’s CPI is stable because the inflation is being routed into balance sheets and asset prices, not consumer baskets. The gap between official “price stability” and the lived experience of currency dilution is definitional scope, not measurement failure.

The FX Reserve Mirror

Taiwan’s FX reserves stood at $596.886 billion at the end of March 2026, per the CBC’s April 7 release. The single-month decline of $8.601 billion was the largest since the September 2011 European debt crisis, driven primarily by net foreign capital outflows of $24 billion in March (a record). The CBC entered the market to maintain orderly conditions.

Even after the drawdown, $596.886 billion places Taiwan fourth globally, behind only China, Japan, and Switzerland.

Per capita, the comparison sharpens. Japan, with a population of roughly 124 million and reserves of $1.16 trillion, sits at approximately $9,400 per capita. Taiwan, with 23 million people, exceeds $25,000 per capita. Relative to economic size, Taiwan’s reserve density is far higher than Japan’s.

This is the cumulative ledger of how many USD the central bank has purchased, not evidence of national thrift. Each dollar in reserves corresponds to TWD released into the system. FX reserves and M2 expansion are mirror images of the same intervention history: the foreign-asset side and the domestic-liability side of one ledger.

The CBC is not blind to where the residual liquidity flows. As of late 2025, the CBC has implemented its seventh round of selective credit controls, supplemented by moral suasion directing banks to self-manage real estate loan ceilings. The existence of this toolkit is direct evidence that the CBC understands what would happen if FX-intervention-released TWD flowed unimpeded into property markets, namely the political consequence of an unaddressed housing inflation. The CBC manages downstream. The upstream constraint, the exchange-rate policy itself, remains structural.

From Taiwan to the Global Frame

Carmen Reinhart and M. Belen Sbrancia’s 2011 NBER working paper The Liquidation of Government Debt defined financial repression as the combination of three policy tools used to gradually liquidate sovereign debt:

Real negative interest rates: nominal rates held below inflation, slowly eroding the purchasing power of cash and low-risk fixed-income holdings

Capital controls and financial regulation: friction that limits capital flight from the domestic system

Captive audiences: pension funds, insurers, and banks regulatorily required to hold sovereign debt

Reinhart and Sbrancia estimated that financial repression contributed an annual implicit tax of 3–4% of GDP during the post-war U.S. and U.K. deleveraging cycles, and was the primary mechanism of debt reduction.

The framework solves an otherwise counter-intuitive puzzle. Why has 2–3% inflation paired with 1–2% deposit rates become the post-2008, post-COVID norm across the United States, Japan, the eurozone, and Taiwan, rather than the exception? In my reading, this configuration is a feature of the system, not a bug.

Sovereign debt loads (explicit and implicit, including unfunded social commitments) in major economies have reached levels incompatible with normalized real interest rates. Per IMF World Economic Outlook (October 2025): U.S. general government debt at roughly 124% of GDP; Japan above 230%; the eurozone at 88.2% per Eurostat Q2 2025. If real rates were to return to pre-1980s levels, the debt burdens of major economies would become unsustainable.

I do not see financial repression as an actively designed conspiracy. I see it as a constraint architecture. It is the equilibrium solution of a high-leverage system. In that equilibrium, holders of cash and low-risk fixed income bear the bulk of the dilution cost.

Taiwan’s M2 expansion is the local realization of this global structure on a small-open-economy substrate. The CBC is the executor of this architecture, forced into the role by the export-led growth model on one side and the limits of sterilization on the other.

One caveat worth marking explicitly. The Reinhart–Sbrancia framework is inducted from historical experience (post-war through the 1980s). Applying it to 2020s Taiwan is analogical rather than directly observational. The CBC is not a textbook financial-repression case in Reinhart’s sense. It does not actively use capital controls to suppress rates and dilute domestic sovereign debt. Taiwan’s structure is closer to passive absorption of currency expansion pressure driven by export surplus. The end-state effects are similar (cash holders are diluted), but the mechanism is not identical. Stating the difference matters more than fitting everything into a single elegant frame.

What Would Falsify This

A structural argument is only as good as its falsification conditions. Five variables would force me to reopen this framework. They sit at different layers of the architecture, and they are bookmarkable on purpose: I expect to come back to this list in twelve and twenty-four months.

The most consequential is the global one. My working assumption is that this regime persists on a foreseeable (decade-scale) horizon. Falsifier: a major-economy sovereign debt restructuring, or sustained positive real rates above 2% in the U.S., Japan, and eurozone simultaneously for two or more years. Either would suggest the leverage constraint is loosening and the equilibrium solution is no longer required.

Closer to home, I expect the CBC will not allow a structural TWD appreciation against USD in 2026. Falsifier: USD/TWD breaks below 28.5 (from roughly 31.6 at end-April 2026, around 9% cumulative appreciation) and holds quarterly average below that level. That would imply the CBC has revealed a different preference set than the one this memo assumes.

On the monetary aggregate itself, I expect Taiwan M2 year-over-year growth to stay above 4%. Falsifier: two consecutive quarters of YoY M2 growth below 4%. That would indicate the upstream pressure has weakened materially, or the CBC has tolerated structurally tighter liquidity.

The pressure source itself can also change. Falsifier: electronics and ICT share of total exports falls by 5+ percentage points for two consecutive quarters. The trigger end of the transmission chain would have shifted, and the framework needs recalibration on inputs even if the architecture holds.

Finally, the FX reserve trajectory. Falsifier: twelve consecutive months of declining FX reserves. The cumulative intervention story would have reversed, and the M2 mirror should follow.

These are structural descriptions, not directional bets. If the falsifiers trigger, the framework itself is wrong, and position sizing within it becomes irrelevant.

Where the Allocator Stands

This memo does not answer “should you hold TWD.” It answers an upstream question: does your balance sheet know which point on the institutional terrain it is standing on.

I see three paths, and each pays a different cost.

One path is to accept currency dilution and own assets with repricing power that track M2 expansion. Equities with structural earnings power, scarce real assets. The cost is short-term volatility plus the execution cost of selection error. This fits allocators with time horizon and volatility tolerance.

A second path is high cash. Trade liquidity for optionality, wait for valuation reset or structural inflection. The cost shows up slowly: chronic purchasing power dilution if the financial repression structure persists. This fits allocators with defined short-term liabilities or specific opportunity setups in view.

The third path is jurisdictional. Move part of the balance sheet outside any single currency-of-record system, and diversify exposure to financial repression intensity itself. Here the cost is execution complexity. Tax structure, hedging, compliance. For allocators without cross-border infrastructure, complexity becomes the tax. For those with it, this is where I personally see the cleanest return on operational sophistication.

There is no dominant path. There is only fit between path and allocator condition. Knowing which cost you are paying, and confirming you have chosen to pay it rather than absorbed it by default, is the substantive question.

This memo ends here.

Time Stamp

Written end of April 2026. Key variables at the time of writing:

M2 outstanding (Feb 2026): NT$68.45 trillion

M2 YoY (Feb 2026): 5.38%

FX reserves (Mar 2026): $596.886 billion (4th globally)

CPI YoY (Q1 2026): 1.23%

Real regular earnings YoY (2025): 1.40%

CBC discount rate: 2.0% (held at March 19, 2026 board meeting)

GDP growth: CBC forecast 7.31% for 2025; first three quarters realized at 7.18%

Export concentration (Jan–Nov 2025): Electronics & ICT 73.7%; U.S. share 30.4% (first-time crossover above mainland China at 26.8%)

Current account surplus / GDP (per CBC response to The Economist): ~16%

Disclaimer

This article reflects my personal investment philosophy. It is not investment advice. Make your own informed decisions.

Miyama Capital manages proprietary capital only and does not solicit external investors.

This memo represents the author’s personal views on macroeconomic conditions, interest rate environments, and asset allocation as of the date of writing. It does not constitute a solicitation, recommendation, or guarantee regarding the purchase or sale of any security, fund, bond, or other financial instrument. Investing involves risk; bond prices, interest rates, foreign exchange rates, and economic/policy conditions may materially affect asset values. Scenarios and instruments discussed may become inapplicable as market conditions change. Readers who make investment decisions based on this memo do so at their own risk, and the author accepts no liability for any gains or losses arising from the use or citation of this material.

Kuan H. Wang Founder & CIO, Miyama Capital

Sources: Central Bank of the Republic of China (Taiwan): Financial Statistics, December 2025 Board Meeting Reference Materials, February 2026 Monetary Policy Framework Operational Strategy Review; Directorate-General of Budget, Accounting and Statistics, Executive Yuan; Eurostat; IMF World Economic Outlook (October 2025); Reinhart & Sbrancia (2011), NBER Working Paper 16893.

About Miyama Capital

Miyama Capital is a California-based proprietary investment firm operating a Quantmental Global Macro strategy: systematic quant, macro conviction. Cross-asset macro framework, tracing transmission from events to execution. AI and quant are extensions of discipline, not substitutes for conviction.

Memos are research notes, not solicitations.

Kuan H. Wang, Founder & CIO