Shadow Chair Warsh: How Rate Cuts and Balance Sheet Reduction Can Coexist

Yield Curve Signals After the Warsh Nomination, Term Premium Expectations, and Three Scenario Frameworks

Executive Summary

Key Takeaways

Markets are pricing a “rate cuts + term premium normalization” combination, not a simple hawk/dove shift

Warsh’s core framework: central banks should set short rates but let markets determine long rates

The transition period (Jan-May 2026) creates asymmetric signal discounting where the shadow chair influences markets without accountability

Most likely path is “cut first, balance sheet reduction later” due to liquidity constraints

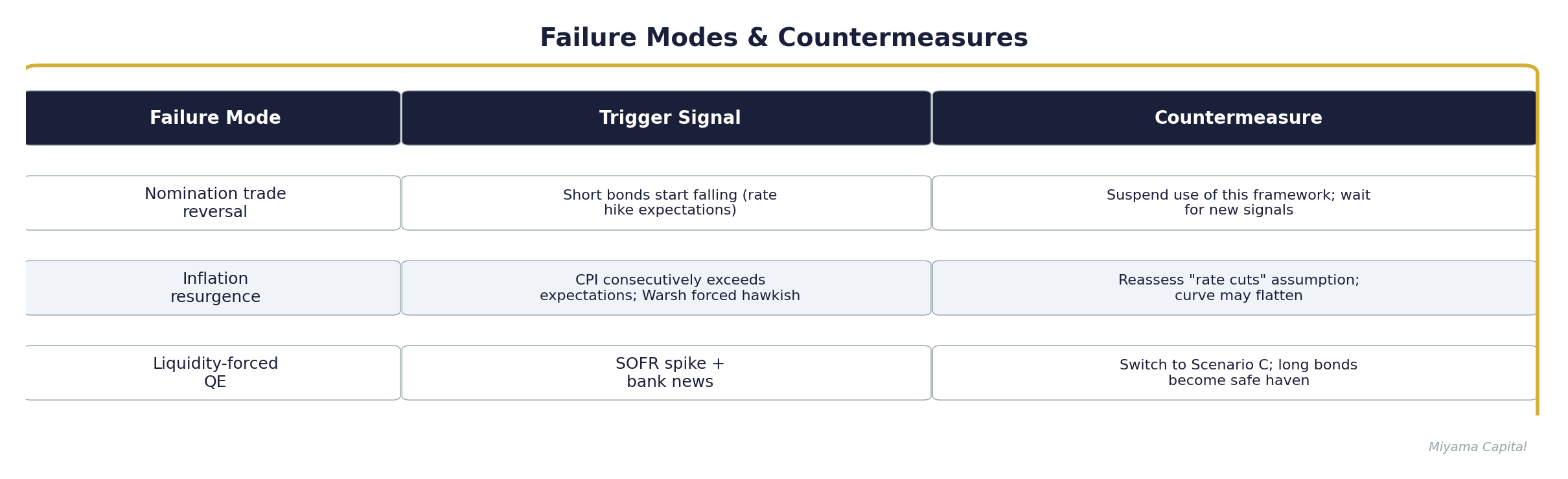

Framework invalidation signal: short and long bonds falling together (yields rising together)

Core Thesis

Markets are attempting to price a “rate cuts + term premium normalization” combination. The short end reflects policy rate reduction expectations. The long end reflects expectations for future balance sheet reduction. During the months between nomination and taking office, Warsh may influence market expectations as a “shadow chair.”

Primary Risks

Liquidity risk (bank HTM losses + reserves approaching lower bound)

Political pressure (Trump prefers low rates, but term premium normalization could push mortgage rates higher)

Non-linear market reactions (if 10Y approaches prior highs, equity panic could turn long bonds into a safe haven)

Watch List

2s10s spread changes (yield curve steepening magnitude)

SOFR vs Fed Funds spread (liquidity stress)

Warsh confirmation hearing language (”gradual” vs “normalization”)

10Y term premium estimates (NY Fed ACM Model)

Framework Invalidation Trigger

If short bonds start falling (rate hike expectations return) while long bonds fall simultaneously, markets have shifted to pricing a “traditional hawk” path. This framework needs revision.

I. The Market Reaction Is a Repricing of Policy Direction

Trump nominated Kevin Warsh as the next Fed Chair.

Markets responded cleanly. Short bonds rallied, long bonds sold off, precious metals fell sharply, and the dollar strengthened.

At first glance, signals appear divergent. The short end is pricing easing. The long end is pricing tightening. If the Fed plans to cut rates, why are long bond yields rising? If the Fed plans to tighten, why are short bond yields falling?

This may not be a contradiction. Markets may be attempting to price Warsh’s policy framework.

The pattern fits the thesis outlined above: short-end yields pricing rate cuts, long-end yields pricing balance sheet normalization expectations. In Warsh’s public commentary, these two things can happen simultaneously.

The yield curve is currently steepening. Short and long ends are being driven by different forces.

The key question: Warsh won’t officially take office until May 15, 2026. The Fed’s official press release explicitly states Powell’s term expires on that date. Powell is still Chair. He still runs FOMC meetings. But markets have already started pricing the incoming Chair’s policy inclinations.

This creates a defined transition window where markets price two competing signal sources. We’ll analyze four things: how to interpret the day’s market signals, Warsh’s policy framework, transition period dynamics, and the real-world constraints he faces.

II. Day-One Signals Point to a “Rate Cuts + Term Premium” Combination

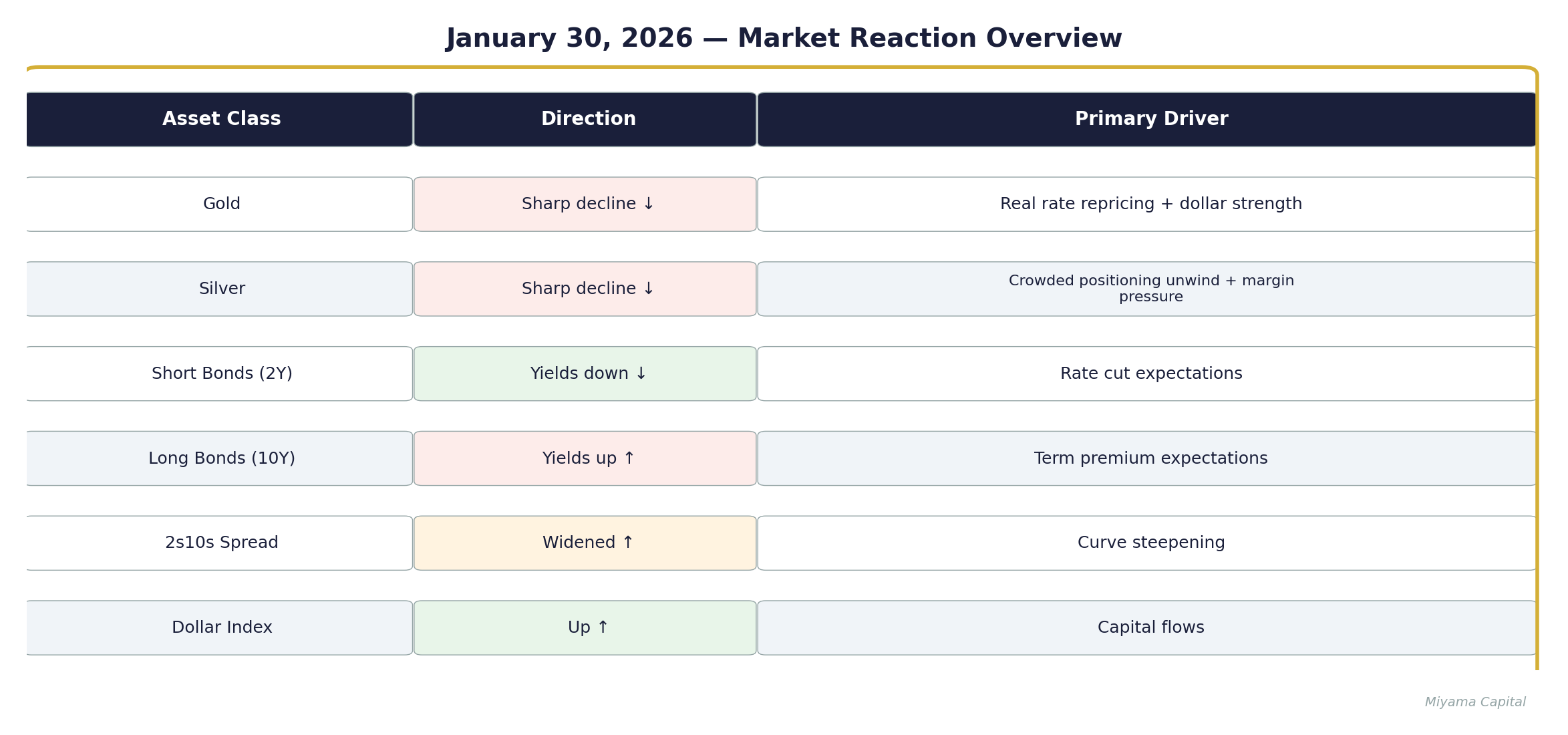

January 30, 2026 Market Reaction Overview

First, the directional moves across major assets.

Source: Barron’s (2026-01-30)

This set of reactions is internally consistent. Markets may be pricing two things.

Rate Cut Expectations Remain Intact

Short bond yields fell. Markets still expect the Fed to cut. This isn’t surprising. Per AP reporting, Warsh has expressed support for lower rates in recent speeches and columns. Markets read him as a candidate who leans toward “short-end easing.” This gives him rhetorical cover to cut.

Trump prefers low rates. Warsh has arguments to accommodate. Markets believe he will cut.

Term Premium Normalization Expectations

Long bond yields rose. This may reflect markets starting to price term premium normalization.

Over the past decade, the Fed bought massive amounts of long bonds through QE, compressing term premium. The “extra compensation” investors require to hold long bonds was artificially suppressed. Warsh’s core argument: central banks shouldn’t distort market pricing.

Reality check: Fed QT has already slowed significantly. Reserves are approaching the “comfort floor.” Warsh is unlikely to restart aggressive balance sheet reduction immediately. But markets price expectations. If Warsh’s philosophy favors term premium normalization, even with delayed execution, long bond risk premiums may move in that direction first.

Precious Metals Crash Requires Multi-Factor Interpretation

Gold and silver posted historic single-day drops. Per Barron’s, gold futures suffered a rare, outsized single-day drop; silver futures saw a sharp drop relative to recent history. This was the day’s most striking phenomenon.

This aligns with the “rate cuts + term premium normalization” framework: if markets believe Warsh can suppress inflation expectations, real rates could rise even as nominal rates fall (rate cuts). That’s bad for gold.

But we need to acknowledge that the precious metals crash likely had multiple simultaneous causes.

Dollar strength: direct pressure on dollar-denominated assets

Leverage and crowded trade unwinding: gold positioning may have been overly crowded; any trigger could cascade into forced liquidation

Futures margin adjustments and liquidity pressure: violent volatility can trigger margin calls, accelerating selling

Risk sentiment shift: markets reassessing risk premiums across asset classes

Treating the precious metals crash as “validation of a single framework” oversimplifies. A more robust interpretation: this is one signal consistent with our framework, but we need to watch dollar moves, real rates, and risk asset behavior going forward to confirm causality.

Suggested verification sequence: first check real rates (TIPS implied), then dollar, then CFTC positioning data.

III. Warsh’s Framework Is “Steep Curve,” Not Simply Hawk or Dove

Warsh Background

Fed Governor from 2006-2011. During the 2008 financial crisis, he was Bernanke’s key liaison to Wall Street. Publicly questioned QE2 in 2010, but ultimately voted yes. Resigned early in 2011, citing dissatisfaction with the Fed’s shift toward “permanent intervention.” Since then: research at Stanford’s Hoover Institution, private investing, and entry into Trump’s advisory circle.

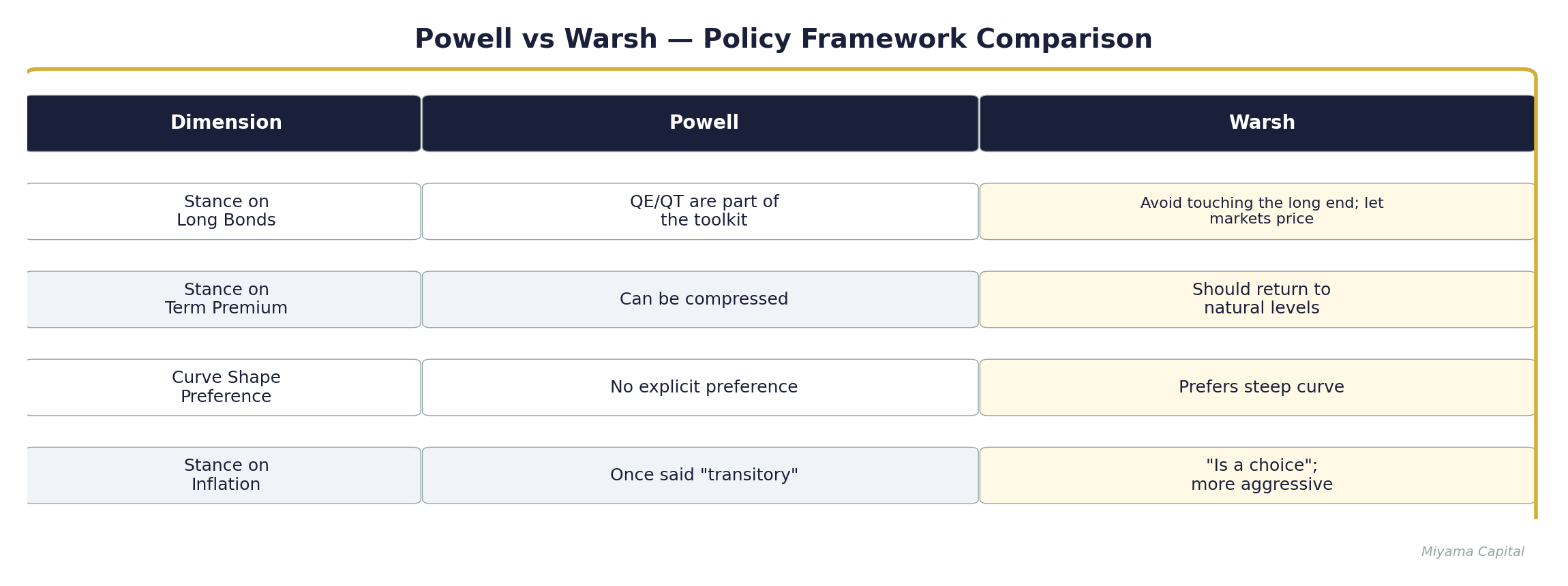

His Core Argument Is About Curve Shape

Warsh’s policy framework can be summarized in one sentence: central banks should set short-term rates, but shouldn’t distort long-term rates.

Traditional central bank operations: the Fed adjusts the fed funds rate (short end) to influence the economy. That’s “normal” monetary policy.

QE-era operations: the Fed didn’t just move the short end. It bought massive amounts of long bonds, directly suppressing long-end yields. The entire curve came under central bank control.

Warsh’s argument: move the short end, let markets determine the long end.

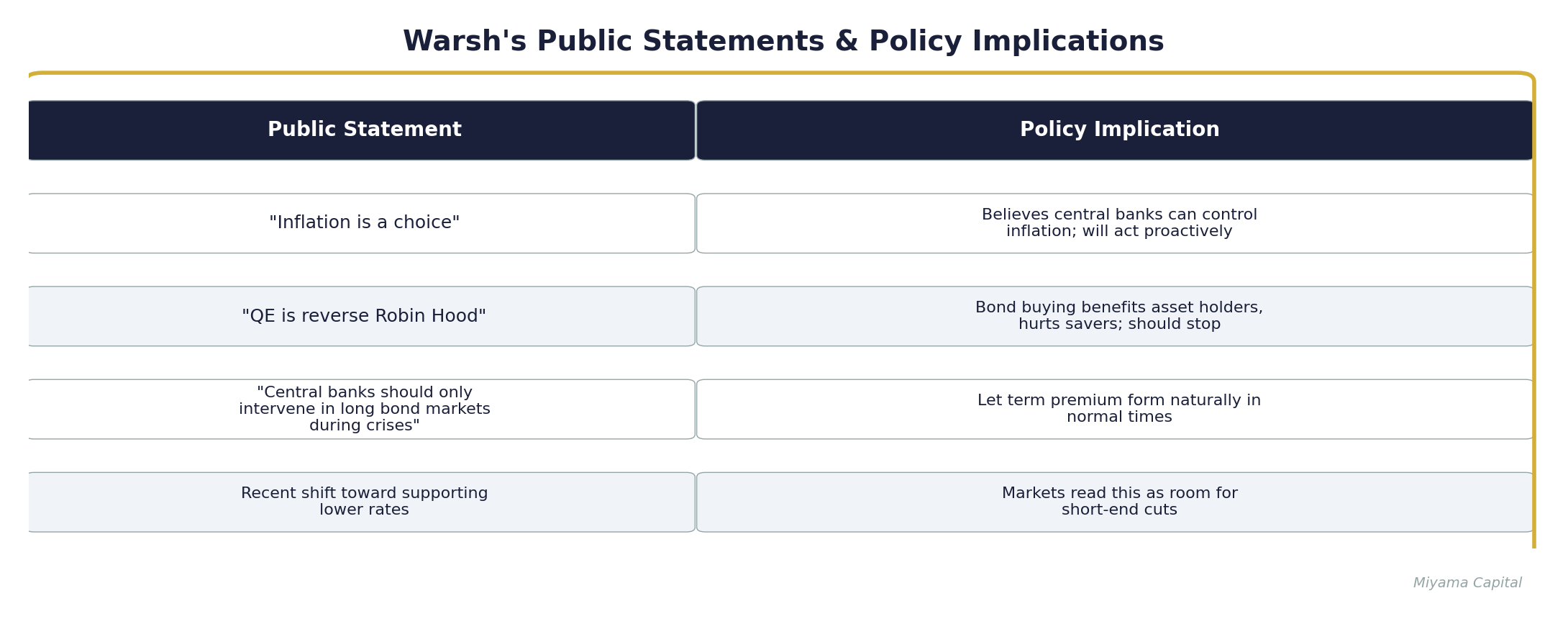

His public statements:

Sources: “Inflation is a choice” from Hoover Institution program/articles; recent stance shift per AP News

“Rate Cuts + Balance Sheet Reduction” Isn’t a Contradiction in His Framework

In Warsh’s framework, these two things can coexist.

Rate cuts: short-term rates should adjust with economic conditions

Balance sheet reduction (or at least no expansion): because central banks shouldn’t distort long-end yields, term premium should return to market pricing

This can’t be described as “hawk” or “dove.” It’s a yield curve shape argument. He wants a steep curve. Short end low (supporting the economy). Long end high (market-determined).

Differences from Powell

The day’s market reaction may have been an attempt to price this difference.

IV. The Transition Period Creates Asymmetric Signal Discounting

Nomination Doesn’t Equal Taking Office

Timeline:

2026-01-30: Trump nominates Warsh

2026-02 to 04: Senate confirmation process (potential delays, political resistance)

2026-05-15: Powell’s term as Chair expires (per Fed official press release)

After: Warsh officially takes office (if confirmed)

Source: Federal Reserve Board (2022-05-23 press release)

Several months of transition lie between. During this period, markets must digest signals from two Chairs simultaneously.

The Incoming Chair Can Talk Without Taking Responsibility

Before officially taking office, Warsh can release signals through public channels: speeches, interviews, policy statements during confirmation hearings.

But he doesn’t need to be accountable for any FOMC decisions. No consequences to face. No execution difficulties to consider.

This creates asymmetry. He can articulate philosophy without bearing execution risk. Yet markets may start pricing his policy inclinations in advance.

Imagine a public company announces a new CEO, but the old CEO has three more months. The board says the new CEO has vision and will reform. The old CEO says he’ll maintain current strategy. Who does the market listen to? Usually, it starts pricing the new CEO’s expectations. This may be Powell’s situation now.

Powell’s Guidance May Be Discounted

In theory, Powell is still Chair. FOMC statements are still his. But markets may have already started pricing the incoming Chair’s policy inclinations. Powell’s guidance may be discounted.

Suppose March FOMC: Powell says “rates unchanged.” Same week, Warsh says publicly “should consider cutting.” How will markets weigh these two signals? This is the core uncertainty of the transition period.

Historical Reference

Warsh has repeatedly mentioned the 1951 Treasury-Fed Accord. That agreement established Fed independence, freeing the Fed from the obligation to peg Treasury yields. If he invokes this historical precedent during confirmation hearings, claiming he’ll push for “balance sheet normalization,” market expectations for term premium normalization could strengthen further.

V. Real-World Constraints

Warsh’s framework is clear. But framework is one thing. Execution is another.

Institutional Constraints: The Fed Chair Has Only One Vote

FOMC voting structure: all 7 Governors have permanent votes. 12 regional Fed Presidents rotate voting rights; 5 vote each year. Total: 12 votes. The Chair has 1.

The Chair’s power comes from “agenda setting” and “consensus building,” not dictating.

One more variable: after his term as Chair expires, Powell can choose to remain as a Governor. Fed official records show Powell’s Governor term runs until 2028-01-31. Whether he stays will affect transition-period power dynamics. If he remains, Warsh faces “the former Chair is still in the room.” Other Governors were mostly appointed during the Powell era. Their positions may not align with Warsh.

How many FOMC members can Warsh convince to support his framework? This isn’t his call alone.

Liquidity Constraints: QT Has Already Slowed Significantly

The lessons from the 2023 SVB crisis remain fresh. The Fed raised rates rapidly, bond prices fell, banks had large unrealized losses in their HTM portfolios. SVB collapsed from liquidity crisis.

Current situation: Fed QT has slowed significantly. Reserves are approaching the “comfort floor.” Banks still have substantial unrealized HTM losses.

This means Warsh is unlikely to restart aggressive balance sheet reduction in the short term. The more likely path: cut rates first, wait for long bond yields to fall naturally and markets to digest, then consider restarting balance sheet reduction. Actual execution may have to wait until 2027.

Liquidity Pressure Transmission Mechanism

If term premium normalizes too quickly, it could trigger a chain reaction. Long bond yields rise, expanding bank HTM losses. Reserves decline, creating Repo market pressure. SOFR vs Fed Funds spread widening becomes the liquidity tightening signal. In this scenario, various assets could move in the same direction. Liquidity pressure would amplify short-term drawdowns.

Political Constraints: What Does Trump Actually Want?

Trump’s public position is clear: he prefers low rates.

But there’s a contradiction here. Warsh’s “term premium normalization” would push long bond yields higher. Mortgage rates track 10Y and 30Y. If 10Y yields approach prior highs, 30-year mortgage rates could return above 8%. That pressures the housing market.

Trump wants low rates. But does he want “all rates low,” or just “short end low is fine”? This question will affect Warsh’s execution room.

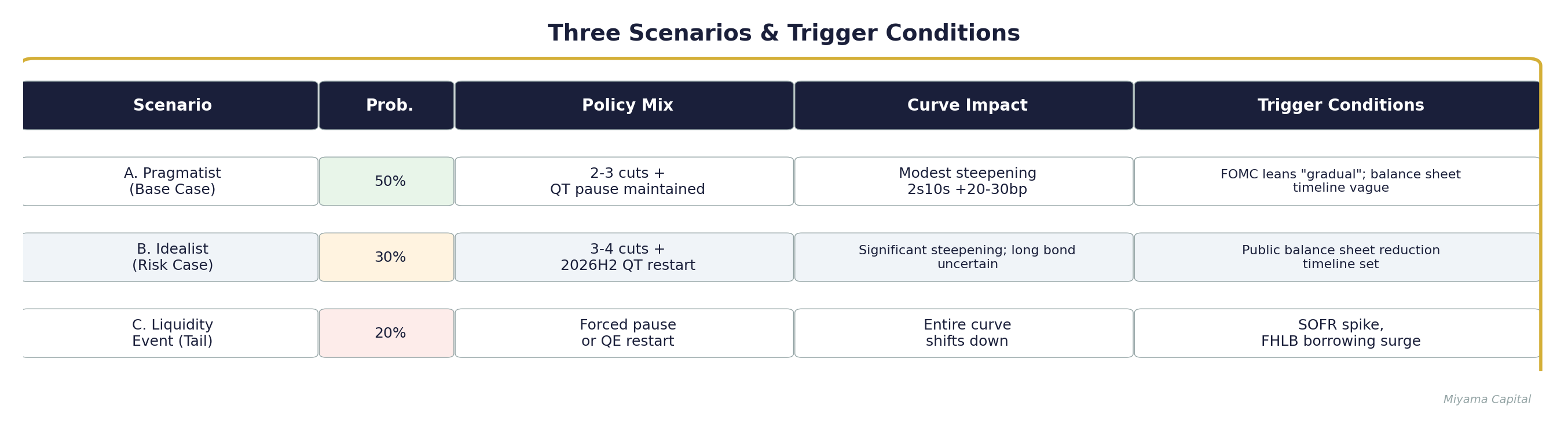

VI. Three Scenarios and Trigger Conditions

Background

Fed QT has slowed significantly. Reserves are approaching the comfort floor. Warsh’s “philosophy” favors term premium normalization, but “execution” faces real-world constraints. The more likely path: cut rates first, consider restarting balance sheet reduction after markets digest.

The probabilities below are subjective estimates based on comprehensive judgment of current market environment and policy constraints. They are not quantitative model outputs.

Illustrative Value Warning

The figures below (bp changes, number of cuts, yield thresholds) are all illustrative values for scenario analysis. They reflect the author’s subjective judgment about current conditions and should not be used directly as trading parameters. Actual thresholds need calibration based on market conditions and individual risk tolerance.

Scenario A: Pragmatist Warsh (Base Case)

Assumption: real-world constraints dominate. Warsh chooses the “cut first, balance sheet reduction later” path.

Observation indicators: whether the first FOMC statement includes language like “gradual” or “data dependent”; whether balance sheet timeline remains vague.

The yield curve will steepen modestly, primarily driven by rate cuts (short end down). Long bond pressure comes from “expectations” rather than “actual balance sheet reduction.” If markets find execution weaker than rhetoric, long bonds may rebound.

Scenario B: Idealist Warsh (Risk Case)

Assumption: inflation continues falling, bank liquidity stays stable, Trump’s tolerance for long bond yield increases exceeds expectations. Warsh can execute his philosophy.

Observation indicators: whether he publicly sets a balance sheet reduction restart timeline; whether he calls for “balance sheet normalization.”

The yield curve will steepen significantly, but long bond direction is highly uncertain. If 10Y yields approach prior highs (reached in 2023), several forces will coexist: equity panic, yield buyers stepping in, long bonds becoming safe havens, capital rushing into short bonds. The primary driver of steepening may keep switching mid-process.

Scenario C: Liquidity Event (Tail Case)

Assumption: even if Warsh merely “says” he’ll restart balance sheet reduction, market pricing alone could trigger liquidity pressure.

Observation indicators: SOFR vs Fed Funds spread widening (warning level illustrative >10bp; danger level illustrative >25bp, needs calibration based on market conditions); bank FHLB borrowing surge; Treasury auction bid-to-cover ratios declining notably.

The Fed would be forced to explicitly commit “no QT restart” or even restart QE. Entire curve shifts down. Long bonds become a safe haven instead.

Update Rules: When to Move from A to B or C

If Warsh explicitly sets a balance sheet reduction timeline during confirmation hearings or first FOMC after taking office, treat as switching from A to B

If SOFR spread exceeds warning level for consecutive days, or bank liquidity event news emerges, treat as switching from A to C

If long bond yields rise rapidly triggering reports of expanded bank HTM losses, or Repo market shows stress, treat as switching from B to C

VII. Observation Indicator Checklist

Short-Term Indicators (Next 3 Months)

For determining “which scenario is materializing.”

[ ] Warsh confirmation hearing language: how does he describe term premium? “Should normalize” vs “gradual adjustment”?

[ ] Powell’s March FOMC statement vs Warsh’s concurrent public statements: consistent direction or contradiction?

[ ] 2s10s spread changes: continued widening supports Scenario A/B; narrowing or reversal requires framework revision (data source: FRED)

[ ] 10Y term premium estimates: continued rise means markets are pricing Warsh’s framework (data source: NY Fed ACM Model)

[ ] Fed Funds futures: rate cut expectations rising but long bonds still falling is consistent with framework (data source: CME FedWatch Tool)

Medium-Term Indicators (After Warsh Takes Office)

For judging “execution intensity” and “liquidity pressure.”

[ ] SOFR vs Fed Funds spread: normal near 0; warning illustrative >10bp; danger illustrative >25bp (data source: NY Fed)

[ ] Bank FHLB borrowing data: sharp increases are liquidity pressure precursors (data sources: FHLB quarterly reports, Fed H.8 report)

[ ] Treasury auction bid-to-cover ratios: declines indicate weakening market absorption capacity (data source: TreasuryDirect)

[ ] Equity reaction when 10Y approaches prior highs: watch whether long bonds become a contrarian safe haven

[ ] Fed balance sheet changes: whether a balance sheet reduction timeline is actually set (data source: Fed H.4.1 report)

VIII. Framework Delivery

Applicable Boundaries

This framework applies to:

Observing yield curve shape changes and underlying drivers

Understanding differences between Warsh’s policy framework and Powell’s

Tracking transition-period signal discounting

This framework does not apply to:

Single-asset directional trades (long bond direction in Scenario B is highly uncertain)

Short-term or intraday trading (this analysis operates on a multi-month time horizon)

Individual stock or sector allocation (this analysis covers only the yield curve)

Operating Rules (Risk Management Posture)

If Warsh confirmation hearing language leans “gradual,” maintain Scenario A assumption; focus attention on whether short-end pricing accelerates

If Warsh explicitly sets a balance sheet reduction timeline, switch to Scenario B; reduce long bond directional exposure; yield curve steepening direction is relatively certain but volatility increases

If SOFR spread exceeds warning levels for consecutive days, increase liquidity preference; wait for Fed response

If 10Y approaches prior highs and equities start falling, watch whether long bonds become a contrarian safe haven; don’t rush directional judgment

If Powell and Warsh signals clearly contradict, expect elevated short-term volatility; reduce overall directional exposure

If short and long bonds fall together (yields rising together), this is a framework invalidation signal; reassess

Failure Modes and Countermeasures

IX. Three Paths and Their Costs

The day’s market reaction direction was clear: short and long ends were driven by different forces, and the yield curve steepened. This aligns with the “rate cuts + term premium normalization” hypothesis, but we need more data to confirm whether this pricing logic persists.

Warsh’s framework is clear, but his execution room is actually quite limited. Much smaller than his rhetoric suggests. The most likely path remains “cut first, balance sheet reduction later.”

Starting today, markets must digest signals from two Chairs simultaneously. Powell’s guidance may be discounted until the handover.

Facing this environment, there are three risk management postures to choose from.

Path A: Observation First

Risk management posture: don’t rush to build directional exposure; continue tracking Watch List indicators; wait for Warsh confirmation hearings to provide more signals

Cost: may miss early yield curve steepening pricing

Suited for: those with lower risk tolerance or doubts about Warsh’s execution capability

Path B: Curve Shape First

Risk management posture: accept the assumption that “yield curve steepening direction is relatively certain, but the driver may switch”; focus attention on yield curve shape changes rather than single-asset direction

Cost: if framework fails (short and long bonds fall together), need to adjust quickly; drawdowns may increase in high-volatility scenarios

Suited for: those who can tolerate volatility, can track multiple key indicators, and are willing to adjust based on signals

Path C: Defense First

Risk management posture: lean toward short duration and low volatility exposure; wait for liquidity risk to release or framework validation before considering increased directional exposure

Cost: if Scenario A or B materializes smoothly, may miss returns

Suited for: those concerned about liquidity risk or who believe markets are overly optimistic

No path is absolutely correct. The choice depends on your judgment of Warsh’s execution capability, your risk tolerance, and your ability to track key indicators.

This isn’t a prediction. It’s just a framework. We don’t know what Warsh will do, but we know how to observe.

The rest? Let the market tell us.

Sources

Powell Chair term expiration date: Federal Reserve Board press release (2022-05-23), explicitly states term expires 2026-05-15

Powell Governor term: Federal Reserve Board official records, Governor term until 2028-01-31

Precious metals decline: Barron’s (2026-01-30), gold futures record single-day drop, silver futures largest single-day drop since March 1980

Warsh “Inflation is a choice” statement: Hoover Institution program/articles

Warsh recent stance shift: AP News (2026-01-30)

10Y yield historical high: Reached prior highs in 2023; exact closing level needs confirmation

Term premium data: NY Fed ACM Term Premium Model

Disclaimer

This memo is for educational discussion and internal-style research notes. It is not investment, legal, or tax advice. Rules and tax regimes change, and outcomes depend on individual facts and jurisdiction. Consult qualified professionals before implementing leverage or tax planning.

Kuan, Founder of Miyama Capital