Iran’s Missiles Did What U.S. Diplomacy Couldn’t

The market is scoring this war wrong. Here’s the structural scorecard.

Kuan, Founder & CIO | Miyama Capital Geo-Macro Series | 2026-03-18

This is the sixth analytical installment in Miyama Capital’s Geo-Macro Series on the 2026 Iran-Israel war (Articles 3 through 8). The methodology across all six pieces is the same: identify directional shifts and layer resolution progressively, recalibrating as data arrives. This installment asks: whose structural position changed permanently?

Key Takeaways

The market is pricing this war on short-term cost (oil above $100, ~200 U.S. service members wounded across seven countries). That scorecard misses the structural gains. The real question: whose position in the Middle East power architecture shifted permanently?

Iran’s missiles did what decades of U.S. diplomacy could not. By striking six Gulf states directly, Iran destroyed its own decade of patient influence-building and pushed every Gulf capital toward the U.S. security umbrella in weeks.

The U.S. captured four layers of structural benefit: military degradation of Iran, economic control via Kharg Island and DFC insurance, security architecture integration with Gulf states, and accumulating negotiation leverage (as of Day 18, the U.S. actively refused Iran’s outreach).

China is the largest indirect loser. Hormuz oil transit collapsed from 5.35 million barrels per day to 1.22 million (Foreign Policy, Day 18 data), Beijing abstained at the UN Security Council instead of vetoing, and every barrel still transiting Hormuz now flows on American financial infrastructure.

All new judgments carry a 12-month verification commitment. If China builds an alternative security architecture (sovereign reinsurance plus naval escort) within 12 months, or Gulf states collectively reject the U.S. framework, this thesis fails. The scorecard is public; accountability is the mechanism.

The Market Is Using the Wrong Scorecard

Oil above $100. Roughly 200 U.S. service members wounded across seven countries as of Day 17, per U.S. military reporting. Iran claiming its weapons arsenal remains “largely intact.” Read that scorecard, and the consensus conclusion writes itself: Trump lost, America is stuck.

I see something completely different.

That scorecard only counts short-term cost. It ignores the power architecture of the Middle East before the war versus after. Measure by that framework, and the answer flips.

The 1973 oil embargo is a useful parallel. At the time, everyone scored it as an Arab victory: oil prices spiked, Western economies took damage. But the long-term effect was the opposite. The embargo accelerated Western investment in energy independence and eroded OPEC’s structural pricing power over the following decade. Short-term pain and long-term structural shift are two different ledgers.

This article scores on the structural ledger. One question only: whose permanent position in the regional order changed?

Iran Vetoed Its Own Decade of Diplomacy

Start with pre-war Iran.

Over the past decade, Tehran built a subtle but effective influence structure across the Middle East through proxy networks and diplomatic repair. The 2023 China-brokered Saudi-Iran normalization was widely read as the signature event of a “post-American” Middle East. Qatar maintained gas field cooperation with Iran while serving as a back-channel mediator. The UAE kept economic ties alive through Dubai trade corridors. Oman played neutral broker. Turkey balanced between Washington and Tehran.

Imperfect, but functional. Iran had friends, or at least neighbors who were not enemies.

Then Iran vetoed all of it in two weeks.

Saudi Arabia’s Ras Tanura refinery and Shaybah oil field were hit; Riyadh intercepted multiple drones. The UAE’s Dubai airport and hotels were struck, an AWS data center was destroyed, and on Day 17 Dubai airport suspended flights again after another drone fire. Bahrain’s desalination plant was hit. A U.S. base in Kuwait was struck, killing four American service members. Qatar’s LNG facilities were attacked, its airspace closed, and four ballistic missiles were intercepted. Oman’s Sohar port took collateral damage, two people killed. The IRGC publicly threatened Saudi Arabia, declaring U.S. carriers in the Red Sea a “direct threat.” (Attack data through Day 17, compiled from official government statements, Alma Research Center, and Human Rights Watch reporting dated March 16.)

The countries that got hit responded by writing America’s condemnation resolution for it. UN Security Council Resolution 2817, drafted by Bahrain with an unusually high number of co-sponsors, passed 13-0-2 with China and Russia abstaining (UN Security Council vote record, March 7, 2026). In the recent context of Middle East diplomacy, that alignment is remarkable.

Why did Iran play the game-theoretically suboptimal move? Trump himself admitted “nobody thought they were going to hit Gulf countries” (White House press conference, March 14, 2026). Plausible explanations include the IRGC’s mosaic defense structure allowing provincial commanders to act independently, central coordination collapsing after the Supreme Leader was killed, or “strike everyone” simply being the IRGC’s default mode when ideology overrides strategic calculation. Regardless of the cause, the outcome is identical: Iran went from “leader of the resistance axis” to regional aggressor.

Four Structural Gains for the U.S.

The market is tallying America’s short-term costs. I am tallying its structural gains.

Structural Gain 1: Military Degradation

Khamenei was killed in a joint U.S.-Israeli strike. The IRGC’s organized military capability sustained severe damage, including hits on nuclear facilities. If current public battle damage assessments are roughly accurate, the reconstruction timeline extends to five to ten years. The operative threshold is degradation sufficient for insurance companies to return to the market. Full disarmament is unnecessary.

As of Day 18: Ali Larijani, secretary of Iran’s Supreme National Security Council, was killed alongside Basij commander Soleimani in a targeted strike. Israel’s defense minister stated the campaign to “continue hunting” remains active. Most analysts classified Larijani as a pragmatist. His elimination compresses the diplomatic space for any negotiated settlement and signals continued erosion of Iran’s command hierarchy. (Sources: CNN, IRGC-affiliated media confirmation, Israeli MOD statement, Day 18.)

Structural Gain 2: Economic Control

Kharg Island’s oil infrastructure is physically intact, but its military defenses are gone. That makes it a permanent hostage. Combined with the DFC insurance monopoly analyzed in Article 7, the U.S. now controls Iran’s economic lifeline while simultaneously setting the cost structure for Hormuz transit. Roughly 20% of global seaborne crude passes through the strait, though the exact share varies by statistical methodology.

Structural Gain 3: Security Architecture Integration

All six Gulf states pivoted from “balanced diplomacy” to the U.S. security umbrella, though the depth of pivot varies. Saudi Arabia, Bahrain, and Kuwait moved fastest; Oman’s shift is the shallowest, with Sohar port damage being collateral rather than a direct IRGC strike. De facto joint operations are already happening: Bahrain intercepting missiles, Qatar shooting down aircraft, Saudi Arabia downing drones. The contours of a post-war security architecture are forming: institutionalized multilateral escort operations plus arms sale packages.

One counterintuitive detail matters here. The EU foreign ministers publicly declined to extend naval operations to Hormuz (CNN, citing EU foreign affairs council decision, March 16, 2026). Trump publicly criticized allies for not helping (White House statement, same day). But Europe’s absence strengthens the American monopoly. If only the U.S. can provide military escort, the DFC insurance bundle becomes even more irreplaceable. Trump may have been publicly angry at allies while privately welcoming the result.

In 1987, Operation Earnest Will left behind the Fifth Fleet in Bahrain: hardware. In 2026, what remains is DFC insurance plus multilateral escort SOPs plus arms sale contracts: software. Lower cost, deeper control, harder to expel.

Structural Gain 4: Accumulating Negotiation Leverage

Everyone is waiting for the U.S. to decide.

The most significant signal on Day 17: according to CNN citing senior White House sources, Iranian officials reached out to Trump’s Middle East envoy attempting to reopen diplomatic channels. They were refused. As of Day 18, CNN reports the Trump administration lacks confidence that Mojtaba Khamenei actually controls Iran’s command structure, a specific and operationally meaningful reason to decline engagement. The uncertainty over who holds decision-making authority inside Iran is a new data point that raises the bar for any negotiation.

Meanwhile, Foreign Minister Araghchi insisted on CBS News Face the Nation (aired March 15) that “we never asked for a ceasefire or negotiation.” The gap between rhetoric and action no longer requires interpretation.

My read: the U.S. now holds active refusal power. Article 5 assessed that Washington did not need to negotiate. The situation has escalated beyond that. Washington received Iran’s outreach and turned it away. Iran is waiting. China is waiting. The EU is waiting. Gulf states are waiting. Nobody has independent agency. That is what architectural dominance looks like.

Trump confirmed a roughly one-month delay of the Trump-Xi summit, originally scheduled for March 31 to April 2 (Financial Times interview, published March 16, 2026). His stated reason: “because of the war, I want to be here.” The same interview included a direct question about whether China would help reopen the strait, with the implicit message that non-cooperation means further delay. From where I sit, Trump is bringing to Beijing not just “we beat Iran” but “the entire Middle East now operates under our security architecture.”

The Strongest Counterarguments

Before extending the analysis further, I need to stress-test the thesis against its three strongest challenges.

Bear Case 1: Gulf alignment is wartime behavior, not permanent realignment.

This argument has historical support. After the 1991 Gulf War, Gulf states depended on U.S. security while continuing to cultivate relationships with all sides. But 2026 has a structural difference: Iran struck Gulf states on their own soil. In 1991, Iraq invaded Kuwait; the other Gulf states watched from the sideline. In 2026, Saudi Arabia, the UAE, Bahrain, Kuwait, Qatar, and Oman all took direct hits. When your refineries, airports, and desalination plants have been hit by ballistic missiles, the political cost of “balanced diplomacy” rises permanently. Hedging may return, but the threshold for returning to it has been raised by the missiles themselves.

Bear Case 2: China’s structural downgrade is overstated.

A reasonable challenge. China’s economic presence in the Middle East, particularly trade volume and infrastructure investment, will not go to zero because of one war. But my argument targets the foundational infrastructure of the security order being rewritten, with China’s cost structure in the new architecture permanently changed. If the DFC insurance framework becomes institutional, every barrel transiting Hormuz flows on American financial rails. “Temporary setback” does not describe a change at that scale. The observation metric: whether DFC remains operational 12 months after ceasefire, and whether China launches an alternative framework.

Bear Case 3: The U.S. won a crisis manager role, not an order builder role.

This is the most incisive counterargument. “Last-resort insurer during a crisis” and “architect of the regional order” are different things. If the U.S. is needed only during war and forgotten after ceasefire, my thesis overstates the gain. My response points to the 1987 precedent. After Operation Earnest Will ended, the U.S. did not leave. The Fifth Fleet remained in Bahrain and is still there today. What this war leaves behind runs deeper: DFC insurance, escort SOPs, arms sale contracts. Each carries institutional inertia. But if Gulf states collectively reject the U.S. security framework within 12 months of ceasefire (invalidation condition #2), this argument collapses.

All three counterarguments carry real weight.

I have incorporated them into the invalidation conditions and observation metrics below, and time will adjudicate.

China’s Middle East Influence Faces Structural Repricing

I am making a structural call here with wide magnitude uncertainty. The direction is clearer than the endpoint.

Start with the diplomatic ledger. The 2023 Saudi-Iran normalization was Beijing’s signature Middle East achievement. Iran striking Saudi Arabia with missiles means China’s brokered outcome now faces re-examination under a new military reality. Beijing abstained on UNSC Resolution 2817, not even needing a veto, signaling that China judged it could not stand with Iran this time. But abstention itself undermines the narrative of “China as a reliable Middle East partner.”

The energy ledger is where the hard numbers live. According to Foreign Policy (Day 18 reporting), oil transit through the Strait of Hormuz collapsed from 5.35 million barrels per day to 1.22 million, with nearly all of the pre-war volume originating from Iran. Tehran has offered yuan-denominated passage as a condition for transit, an offer that further entangles Chinese energy security with Iranian military decisions.

The U.S.-China Congressional Commission’s latest reporting adds another layer: Chinese arms transfers to Iran, including attack drones and what appears to be near-finalized anti-ship cruise missile deals plus sodium perchlorate shipments, have been exposed. This guts the “neutral mediator” narrative in a single data point.

The summit delay dynamics are worth tracking. Trump delayed the summit to apply pressure, not to punish. China’s value as a Middle East intermediary shrinks in lockstep with Iran’s bargaining position. Every additional month of delay lowers the price Beijing can negotiate. China’s Ministry of Foreign Affairs responded by emphasizing the “irreplaceability of head-of-state diplomacy” (NBC News, citing MFA regular press conference, March 16, 2026). The tone is conciliatory; Beijing wants to preserve the summit. And on Hormuz specifically, Trump publicly demanded Chinese help reopening the strait, creating a two-cost structure: compliance means joining the American team; refusal means oil prices keep hurting China’s own economy.

My assessment: this exceeds “China hitting a temporary rough patch in the Middle East.” The U.S., Gulf sovereigns, and Lloyd’s syndicates are collectively rebuilding the security infrastructure of Middle East order on American financial rails. Every new DFC policy, every arms sale contract, every escort SOP raises the cost for Beijing to compete in the new architecture. That cost escalation takes time to play out, and the final equilibrium is uncertain.

Market Implications: Beyond the Oil Price

For allocators, this war has reset the long-term pricing logic across two dimensions: energy costs and military procurement. A third area, infrastructure investment in non-Hormuz routes, is an emerging consequence. Each deserves separate treatment.

Permanent energy security premium. Before this war, Hormuz risk was priced as a tail event with a near-zero risk premium; Brent’s geopolitical premium historically fluctuated in the $1 to $3 range. That is over. Hormuz has been proven attackable, and an attacker does not need to close the strait to paralyze the insurance market. Actuarial models will remember this permanently.

Even if supply fundamentals return to surplus, Brent likely embeds a structural security premium in the $5 to $10 range going forward. The $5 end of that range assumes rapid strait reopening, stable DFC framework operations, and progress on alternative route investment. The $10 end assumes slow reopening, continued insurance market hesitancy, and lagging alternative infrastructure. EIA’s near-term forecast projects prices above $95 for the next two months, declining below $80 by Q3, and approaching $70 by year-end. Separately, the IEA flags this as the largest supply disruption on record, with at least 10 million barrels per day of production offline. The EIA’s projected decline trajectory aligns with the “leaky valve” thesis from Article 5. Regardless of where the premium settles, a return to the pre-war near-zero geopolitical premium is a low-probability outcome.

Air defense procurement cycle. All six Gulf states need air defense upgrades: THAAD, Iron Dome, Patriot systems. These purchases carry ongoing maintenance, upgrade, and training contracts. The revenue stream is structural, not one-time.

Non-Hormuz alternative route investment. Saudi Red Sea port expansion, UAE Fujairah pipeline capacity upgrades, Iraq-Turkey pipeline repair. On Day 17, Fujairah itself, a critical terminal for Hormuz bypass routes, was hit by drone strikes, causing fires at the oil storage complex. This adds a layer: even the alternatives to Hormuz carry new risk. The long-term effect is still to reduce Hormuz’s chokepoint leverage, but the timeline and cost just increased.

Three Paths for Allocators

The previous section described structure. This section describes how to position if you accept that structural assessment.

⚠️ The following paths are framework illustrations for discussing allocation logic. They describe directional reasoning, not specific trade recommendations. Specific tickers and sectors mentioned are examples within the analytical framework, not buy or sell signals. Consult your own research and advisors before any positioning decisions.

Path A: Position for the architecture reset (12 to 24 month horizon).

The logic is straightforward. If the U.S. recaptured architectural dominance over Middle East security, the beneficiary chain is identifiable. Permanent energy security premium favors upstream producers and alternative route infrastructure. Air defense procurement enters a structural expansion cycle. DFC insurance institutionalization favors U.S. financial infrastructure. Directional areas include defense contractors (Lockheed Martin, Raytheon, Rafael), Gulf infrastructure EPC contractors, and Hormuz bypass pipeline and port operators.

The cost: you are betting on a structural judgment that takes 12 to 24 months to verify. If Gulf states revert to hedging after ceasefire, or China builds an alternative security architecture faster than expected, this thesis weakens. Suited for allocators with long time horizons who can tolerate being directionally right but early.

Path B: Trade the oil volatility, skip the structural call.

The premise: regardless of architectural changes, oil prices eventually revert to supply-demand fundamentals. The Brent path from $95-plus back to $75 to $85 was analyzed in Article 5; the leaky valve is pricing in. Short-term trading opportunities exist in the spread between blockade decay expectations and ceasefire probability.

The cost: you forfeit the structural upside. If the Hormuz security premium embeds permanently, you will watch upstream and defense repricings from the sideline after oil reverts to $80. Suited for allocators whose exposure is already large enough and who do not want additional geopolitical beta.

Path C: Acknowledge direction, wait for ceasefire text and hard data.

The starting point is epistemic humility. This article’s judgments are built on trend direction, but magnitude and velocity carry error bars. Ceasefire terms, bilateral security agreement texts between Gulf states and the U.S., and whether the DFC framework actually institutionalizes are hard data points that surface over the next three to six months. Waiting for these anchors before positioning means higher confidence at entry, at the cost of missing the first leg.

The cost: opportunity cost. If structural repricing gets pulled forward after ceasefire, latecomers will be chasing. Suited for institutional allocators who need stronger evidence to clear an internal investment committee, or those whose conviction on the geopolitical framework is not high enough to warrant positioning under uncertainty.

All three paths carry distinct costs, but each beats “do nothing and hope.” Which path depends on your time horizon, existing exposure, and conviction level on this framework.

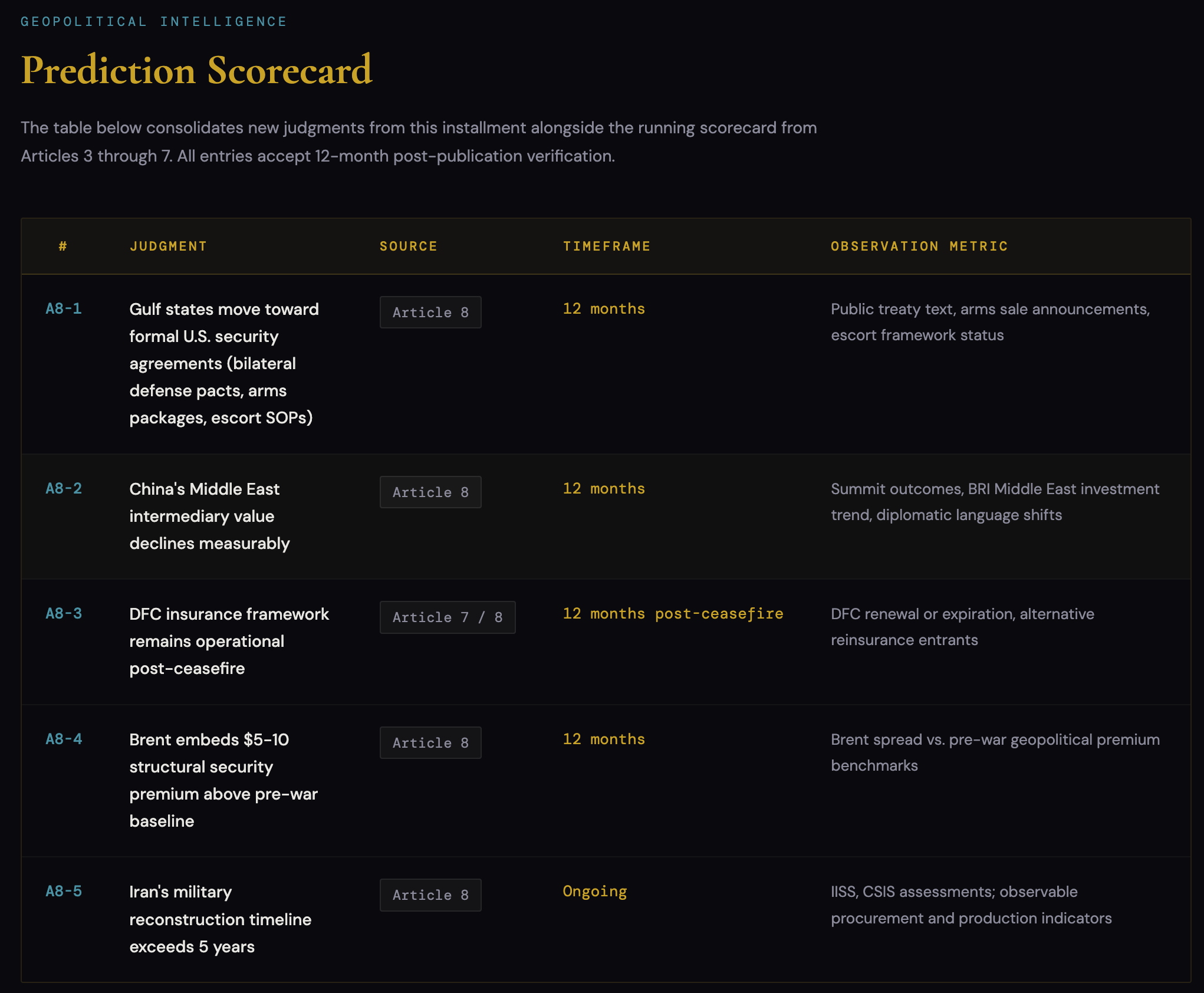

Prediction Scorecard

The table below consolidates new judgments from this installment alongside the running scorecard from Articles 3 through 7. All entries accept 12-month post-publication verification.

Invalidation Conditions (any one triggers framework reassessment):

China establishes an alternative Hormuz security architecture within 12 months (sovereign reinsurance plus Chinese naval escort).

Gulf states collectively reject the U.S. security framework and revert to neutrality.

Iranian regime change produces a pro-Western government, enabling rapid regional diplomatic recovery.

U.S. domestic politics pivot away from Middle East military commitment (e.g., post-midterm Congressional restrictions). Early signal to watch: Joe Kent’s resignation as a Trump-appointed intelligence official, citing his view that Iran does not constitute an imminent threat. This is a data point, not yet a trend.

Watch items: IDF announced large-scale strikes against Hezbollah positions; Lebanon’s northern front is heating up. Not incorporated into the structural thesis at this stage, but warrants monitoring for potential scope expansion.

Methodology Coda

This is the sixth analytical piece in the Geo-Macro Series (Articles 3 through 8). From Day 7 to Day 18, this framework has undergone a full stress test.

The methodology has remained consistent: identify the directional shift first, then layer resolution progressively as data arrives. Recalibrate when the data demands it. Article 3 asked “will this converge?” Article 5 asked “who faces time pressure?” Article 7 asked “how does the blockade leak?” This article asks “whose structural position changed?” Each installment pushes the resolution one layer deeper.

I must acknowledge uncertainty. Geopolitical reordering takes 12 to 24 months to reveal its full contour. The judgments in this article are based on trend direction. I have higher confidence in the direction than in the magnitude or velocity. Both carry wide error bars.

All new judgments accept verification 12 months from publication. That is Miyama’s commitment and this framework’s insurance mechanism. If in 12 months Gulf states have not signed new security agreements with the U.S., or if China’s Middle East investment has actually increased, I will return to review what I got wrong.

Allocators must make decisions when uncertainty is highest, not after consensus forms. This article is a framework for decision-making under uncertainty. A framework’s value depends on internal logical consistency and willingness to submit to verification, not on every individual judgment being correct.

Main text completed as of Day 18; updated with Day 19 developments on March 18, 2026.

Day 19 Addendum (March 18, 2026)

This addendum covers developments on Day 19 that arrived after the main analysis was completed. All three reinforce the structural thesis above; none invalidate it. One adds a qualification worth tracking.

South Pars: Economic control expands from oil to gas.

Israel struck natural gas processing facilities at Iran’s South Pars field, the world’s largest, in a U.S.-coordinated operation (Axios, Jerusalem Post, March 18). Israeli officials confirmed this was the first strike on Iranian gas infrastructure. Early assessments suggest roughly one-fifth of Iran’s gas processing capacity was taken offline (Israel Hayom, citing sources with knowledge of the strike). Structural Gain 2 now extends beyond Kharg Island oil to South Pars gas. The economic leverage surface has widened.

IRGC names five Gulf energy targets by facility.

Hours after the South Pars strike, the IRGC issued a public threat via Tasnim naming five specific facilities for imminent retaliation: Saudi Arabia’s SAMREF refinery and Jubail petrochemical complex, the UAE’s Al Hosn gas field, and Qatar’s Ras Laffan refinery and Mesaieed petrochemical complex (Al Jazeera, Argus Media, March 18). This is the thesis from Section 2 playing out in real time. Iran is doubling down with named targets rather than recalibrating after striking Gulf states. Each additional threat pushes Gulf capitals further from any return to balanced diplomacy.

A qualification on Gulf alignment.

Qatar and the UAE publicly condemned the South Pars strike. Qatar’s foreign ministry called it “a dangerous and irresponsible step,” noting that South Pars is an extension of Qatar’s own North Field (Qatar MFA statement via Al Jazeera, March 18). The UAE issued a rare rebuke calling the strike a “dangerous escalation” (Euronews, citing UAE foreign ministry statement, March 18). This does not reverse Gulf security alignment with the U.S., but it clarifies the texture: Gulf states are accepting American defense while refusing to endorse every Israeli action. The alignment is security-driven, not ideological. Allocators should expect this pattern to persist: operational cooperation with Washington, rhetorical distance from Jerusalem.

Brent at $110.

Brent surged 6.3% to $109.95 following the South Pars strike and IRGC threat (Bloomberg, March 18). This is a short-term spike driven by event risk, not a revision to the $5 to $10 structural premium assessed in the main text. The structural premium is a post-ceasefire equilibrium estimate; $110 Brent reflects active wartime disruption. The distinction matters for positioning: Path B allocators trade the spike, Path A allocators look through it.

Gabbard testimony: “intact but largely degraded.”

DNI Tulsi Gabbard told the Senate Intelligence Committee that the Iranian regime “appears to be intact but largely degraded” (CBS News, Washington Post, March 18). Her written testimony stated Iran’s nuclear enrichment program was “obliterated” after last summer’s strikes with “no efforts since then to rebuild,” but she omitted this line from her oral testimony (Bloomberg, The Hill, March 18). CIA Director Ratcliffe separately stated Iran “posed an immediate threat” before the war, directly contradicting resigned NCTC director Joe Kent’s position. The IC assessment aligns with Prediction A8-5 (reconstruction timeline exceeding five years). The gap between written and oral testimony is a domestic political signal, not an intelligence revision.

Lebanon front escalation.

Israel announced plans to strike Litani River bridge crossings and issued evacuation orders for all civilians south of the Zahrani River (IDF statement via ABC News, Euronews, March 18). This exceeds the “watch item” noted in the main text. A full-scale ground operation to seize territory south of the Litani River is now underway, with Israeli officials comparing the scope to Gaza operations (Axios, March 14). This opens a resource allocation question for the U.S. and a domestic political variable that bears monitoring, but it does not alter the Iran-centric structural thesis at this stage.

Updated prediction status: No existing predictions invalidated. No new predictions added. Observation metrics remain unchanged.

Disclaimer

This article reflects my personal investment philosophy. It is not investment advice. Make your own informed decisions.

Miyama Capital manages proprietary capital only and does not solicit external investors.

This memo represents the author’s personal views on macroeconomic conditions, interest rate environments, and asset allocation as of the date of writing. It does not constitute a solicitation, recommendation, or guarantee regarding the purchase or sale of any security, fund, bond, or other financial instrument. Investing involves risk; bond prices, interest rates, foreign exchange rates, and economic/policy conditions may materially affect asset values. Scenarios and instruments discussed may become inapplicable as market conditions change. Readers who make investment decisions based on this memo do so at their own risk, and the author accepts no liability for any gains or losses arising from the use or citation of this material.

Kuan, Founder & CIO, Miyama Capital