Infrastructure Is the Negotiating Table, and There’s Only One Exit

Five paths, one door. Why Iran’s only security guarantor is the country bombing it.

Kuan H. Wang | Miyama Capital CIO

Miyama Geomacro Series, Art. 16-17 (Combined English Edition) 2026-04-03

Executive Summary

B1 bridge was not escalation. It was Trump’s first term sheet. Every target on the strike list maps to a deal condition: bridges are warnings, power plants are deadlines, oil infrastructure is the nuclear option.

Hormuz is already reopening through five parallel paths. On April 2, JMIC reported 12 ships transiting the strait (pre-war average: approximately 138 per day), and France-linked CMA CGM became the first Western-associated vessel to pass since the war began. Recovery is under 10%, but the gradient is moving.

The real signal from B1 is the second strike, timed roughly an hour after the first, after rescue crews arrived. The Infrastructure Trap works in three layers: cut the supply line, force the IRGC to move into the open, then eliminate the capacity to rebuild. “Stone Age” is a doctrine, not a soundbite.

Iran faces a retaliation paradox. Every strike on Gulf infrastructure pushes Gulf states closer to the US, not further away. Bahrain has introduced a UN resolution authorizing the use of force to reopen the strait. The UAE foreign minister has publicly rejected coercion. Iranian retaliation against regional targets functions as an involuntary recruitment campaign for the American coalition.

April 6 is an accelerator, not an escalation point. Base case 60-65%: if the power grid goes dark and Iran’s launch frequency drops to single digits per day, a mid-April exit window opens. The binding constraint is whether Iran’s organizational capacity survives past the next ten days.

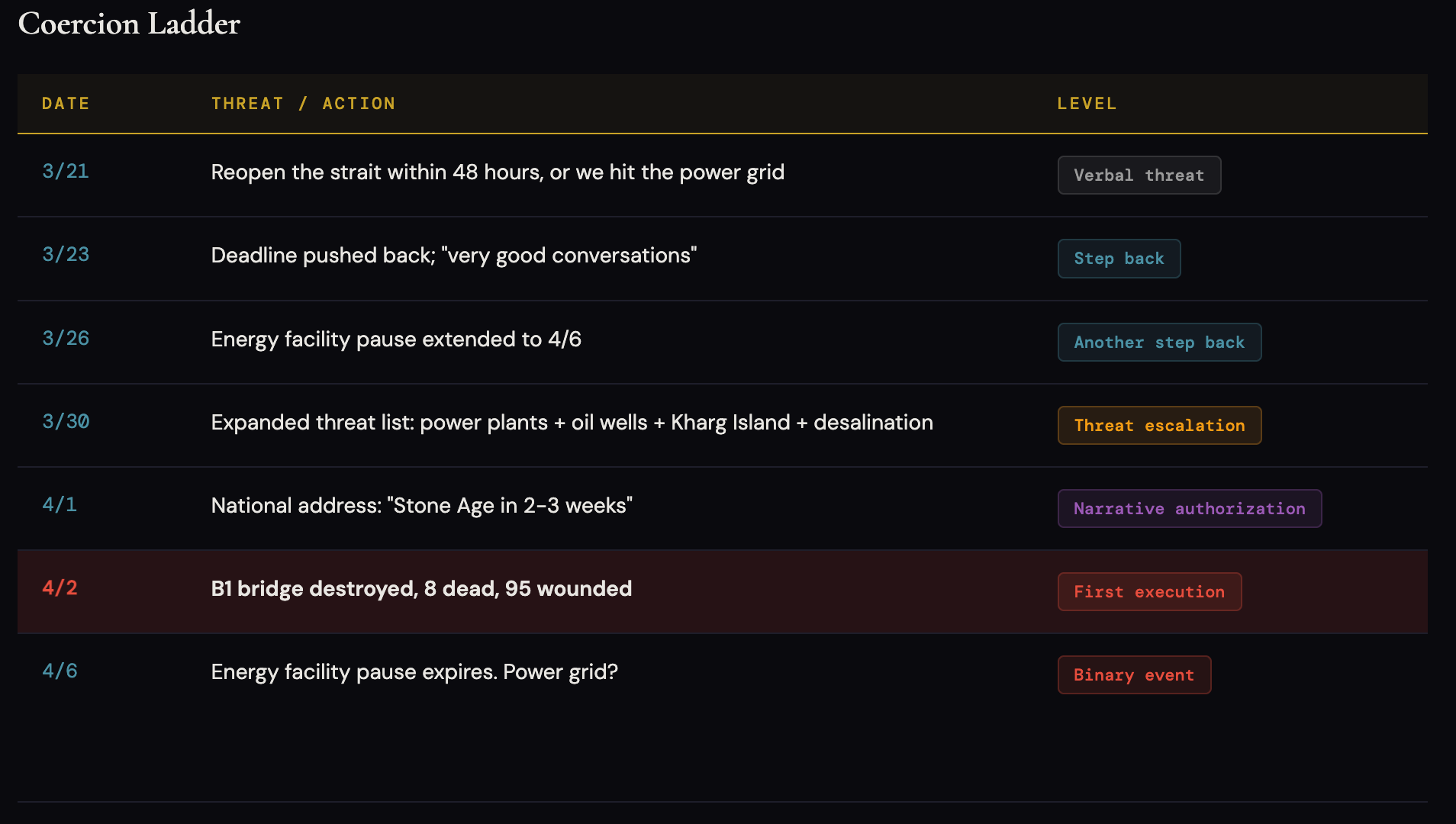

1. The Speech Was Authorization, B1 Was Execution

April 1, national address. April 2, B1 bridge destroyed. Less than 12 hours.

While media outlets were still parsing the speech transcript, the strike was already underway. Trump repeated four points he had already made: the war is necessary, the US is winning, operations must continue, it will end soon. Most coverage interpreted this as “nothing new.” That reading is too shallow.

The speech was not directed at Iran. It was a pre-authorization memo for the American electorate, wrapping a major escalation inside an “almost over” narrative frame. Classic narrative laundering.

Coercion Ladder

Updated after initial filing: On 4/3, Trump warned “hasn’t started yet”; IDF killed missile commander Atimi in Kermanshah.

Every target corresponds to a deal condition.

Read the table from the bottom up. April 6 is the next decision node. The energy facility pause expires that day, and Trump’s April 1 speech has already secured the political license to act. My read: the speech was the authorization. B1 was the first invoice.

2. They Are Not Playing the Same Game

After B1, most analysis focused on whether Iran would retaliate. The framing itself is wrong.

One JDAM breaks a bridge. Iran needs roughly 50 Shaheds to shut down Dubai’s airport for a day. The economic damage might be comparable. The logic is entirely different. Without understanding this asymmetry, you cannot correctly assess where the escalation ladder goes.

The American side runs precision infrastructure economics. B1 was a demonstration. Air superiority plus precision-guided munitions means one or two weapons can sever a bridge’s load-bearing structure. Publicly available estimates put the per-strike cost in the hundreds of thousands of dollars. The collapsing bridge footage hit Truth Social within hours and was amplified rapidly. The timing and method look deliberate, designed to serve both the military objective and the political narrative simultaneously.

Iran cannot replicate this. Ballistic missiles have a circular error probable measured in tens to hundreds of meters. A bridge is a linear target, maybe 20-30 meters wide. The hit probability is inherently low. Cruise missiles are accurate enough but inventories are limited and have been burning down for 34 days. Shahed drones carry 40-50 kg warheads, not enough to crack reinforced concrete bridge piers. Under Israeli and American air defense coverage, concentrating 5-10 cruise missiles on a single structural span is operationally implausible. Iran’s threat to destroy regional bridges is deterrence, not an operational plan.

Iran’s real capability lies elsewhere. Not bridges. Soft targets: oil tankers, port facilities, data centers (an AWS facility was struck on March 1), undefended industrial zones, airport fuel depots (Kuwait was already hit). Iran’s leverage has never been symmetric strike capability. It is the ability to force the entire world to share the cost.

I want to be precise here. The analysis above does not mean “Iran is weak.” Quite the opposite. Anyone who underestimates Iran’s capacity to externalize costs will make the same mistake as those who underestimated the Hormuz blockade itself. Iran’s strength is not in matching strikes. It is in making everyone else pay.

The retaliation paradox. This is the part I think most observers are missing. When Iran strikes Gulf infrastructure, the political consequence runs in the opposite direction from what Tehran intends. Hit a Kuwaiti refinery, a Bahraini power plant, an Abu Dhabi gas facility, and what happens? Gulf states become angrier at Iran, more dependent on American air defense, and more willing to support the US campaign to its conclusion. The US receives more international backing to keep going, not less.

This is already visible. Bahrain has introduced a UN resolution authorizing the use of force to reopen the strait. The UAE foreign minister publicly stated that coercion is unacceptable. Every Iranian retaliation against Gulf infrastructure is an involuntary recruitment campaign for the American coalition. The harder Iran hits regional targets, the stronger the political mandate for Washington to finish the job.

3. The Infrastructure Trap: Three Layers

Most people are counting items on Trump’s target list.

The real signal is not on the list. It is in B1’s second bomb.

Start with the bridge. On the surface, the objective is cutting supply lines. But the deeper effect is forcing the IRGC into a binary choice.

Then comes the forced movement. With the bridge down, IRGC hardliners have two options. Option A: stay put. Western launch sites lose their supply lines, missiles run out, and strike capability goes to zero on its own. Option B: move. Reroute missiles via alternative roads. But missiles in transit are maximally vulnerable. Fixed launch sites have bunkers, camouflage, dispersed deployment. Once a transporter is on a truck moving down an open highway, it becomes a slow-moving linear target with no air defense cover. The American ISR architecture, from satellites and drones to E-8 JSTARS and the recently deployed EA-37B electronic warfare aircraft, is purpose-built for exactly this scenario: tracking and eliminating high-value targets in motion.

IRGC picks A or B, the missile capability goes to zero regardless. The difference is timing.

The third layer is the one that matters most. According to Iranian state television, B1 was struck twice, approximately one hour apart. The second strike came after rescue personnel had arrived on scene (source: Fars News, April 2). The operational logic goes beyond road denial. It communicates that this route is under continuous surveillance, and any repair activity is itself a target.

Trump said “bomb them back to the Stone Age.” That is his political language. What concerns me is the operational doctrine underneath.

Destroying infrastructure is Day 1. Destroying the capacity to rebuild infrastructure is Day 2. “Stone Age” does not mean a country without bridges. It means a country that cannot rebuild bridges. This is not rhetoric. It is a systematic approach to eliminating Iran’s organizational capacity layer by layer.

Post-filing update (April 3): The IDF announced it killed Iran’s ballistic missile forces commander Makram Atimi and several battalion-level commanders in the Kermanshah region (source: IDF statement / Jerusalem Post, April 2). Beyond the three-layer trap, a fourth dimension is emerging: decapitation of the command chain. Supply lines cut, movement punished, repair monitored, and now the officers issuing orders are being eliminated.

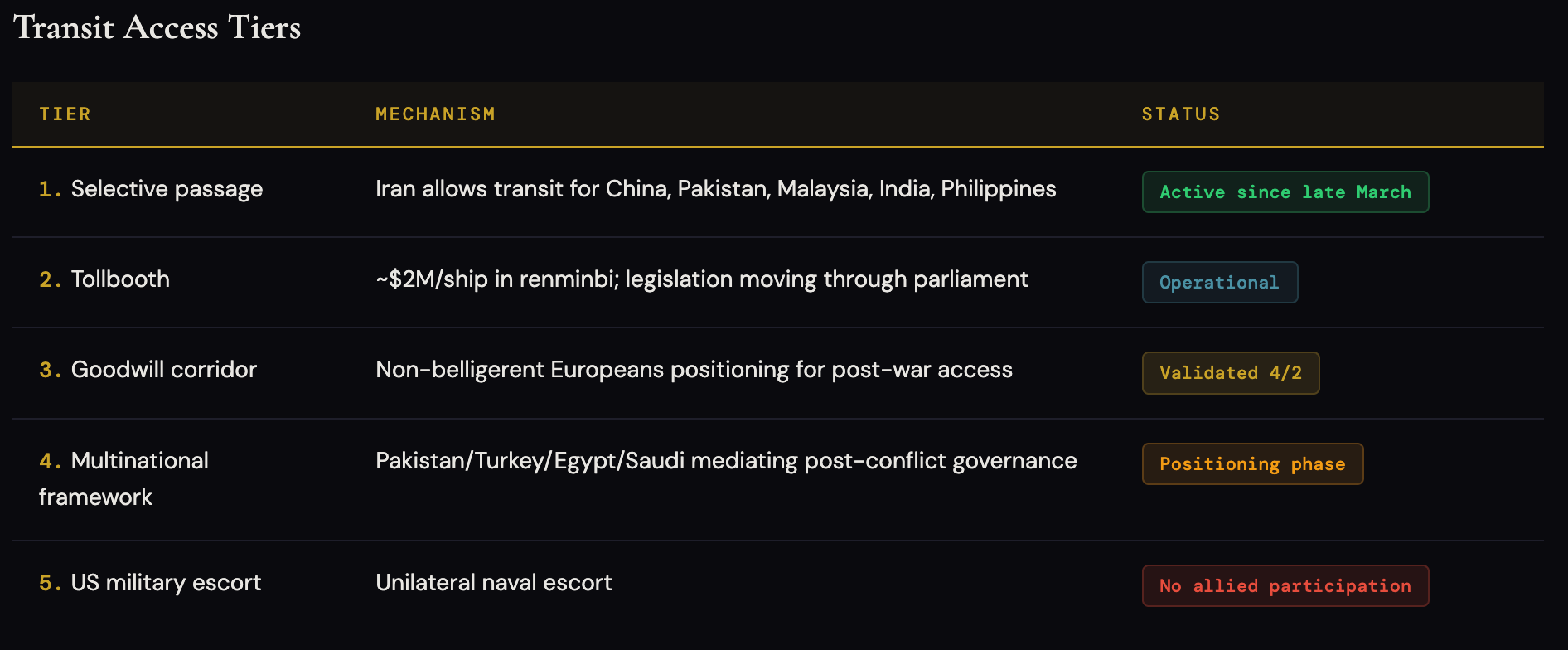

4. Five Paths to the Same Exit

Before going further into the endgame, a question needs answering. If Hormuz is blockaded and infrastructure is being destroyed, why has the market not collapsed?

Part of the answer is that Hormuz is already reopening, through five parallel paths advancing simultaneously. No single path is sufficient. But they do not need to be. They reinforce each other.

The third tier deserves attention because it just activated in real time. On April 2, a CMA CGM vessel, France’s flagship shipping line, transited the strait. The same day Macron publicly criticized America’s military approach. I predicted this tier would activate within days. Two days later, it did. The diplomatic positioning converted directly into transit access.

Real-time validation. On April 2, the Joint Maritime Information Centre (JMIC) reported 12 ships transiting the strait publicly. Pre-war daily average was approximately 138 ships (source: JMIC). That is a recovery rate of roughly 9%. The clearance list has been expanding steadily: China, Russia, India, and Pakistan from March 26; UN humanitarian vessels from March 27; the Philippines from April 2.

But the cold water is necessary. Twelve ships against a pre-war baseline of 138 is not recovery. It is a controlled trickle, and the ships transiting are overwhelmingly from “friend list” countries. The real bottleneck is insurance. Protection & Indemnity Club war risk premiums have not come down. Until they do, most commercial shipowners will not risk the transit regardless of what flags Tehran waves through. Approximately 400 ships remain anchored in the Gulf of Oman waiting for resolution (source: Al Jazeera). Clearing that backlog will take months. Meanwhile, rerouting alternatives are hardening: Iraqi crude via Syria, Saudi exports via the Red Sea, increased US exports to Asia. Some of that demand is not coming back.

Why the market has held. Fed repo facilities are near zero utilization. Dollar swap lines have not been activated. The DXY moved from 98 to 100, far short of a typical dollar shortage signal. The market is pricing in gradient reopening, a progressive normalization rather than a binary open/close. But here is the risk that keeps me cautious: precisely because the market has not priced in the worst case, any deviation from the base case will trigger repricing that is disproportionately violent.

5. The Tollbooth Is Desperation, Not Leverage

Everyone is analyzing how long Iran can keep fighting.

Financing is the binding constraint, not inventory. Who pays to rebuild what the US is destroying?

The answer is nobody.

Revenue has collapsed across every channel. Oil cannot be exported because the Hormuz blockade cuts both ways. Even if it could be sold, the money cannot get in. SWIFT sanctions plus frozen accounts have shut down nearly all payment corridors. Overseas assets are frozen. Multiple think tanks estimate the total at $100-120 billion (sources: Congressional Research Service and Foundation for Defense of Democracies; figures vary by methodology). US courts have awarded over $53 billion of those frozen assets to families of terrorism victims (source: Reuters, cumulative through end of 2025).

Expenditures cannot be controlled. War consumption is accelerating. Infrastructure repair costs are astronomical, assuming repair is even possible under continuous surveillance. The domestic economy is collapsing; Tehran suppressed large-scale protests as recently as January. The proxy network still needs funding: Hezbollah, the Houthis.

The tollbooth’s real motivation. The reported $2 million per ship, settled in renminbi, tells you everything. Dollar accounts are frozen. Euro channels are closed. The only payment corridor still functioning runs through China. This also explains why the cleared ships are predominantly Chinese. It is not political goodwill. China is the only buyer that can actually transfer money to Iran.

The tollbooth is not a weapon the IRGC discovered. In my assessment, it is the last revenue stream of a state whose every other income source has been severed.

6. Trump Wants Fast, But Does Not Need Fast

Trump’s hand is stronger than the surface data suggests.

Most analysis reads declining approval ratings and rising oil prices as evidence that Trump is under pressure to wrap this up quickly. The data points are correct. The framework is wrong.

According to YouGov’s March 27-30 survey (published March 31), overall war approval stands at 28%. Among Republican voters, support dropped from 76% to roughly 61% in a single month. Brent crude surged above $110 following the B1 strike, trading in the $108-112 range as of April 2 intraday (sources: Oilprice.com / Fortune). The national average gasoline price has broken $4 per gallon (source: AAA, April 2).

These numbers mean Trump has motivation to close quickly. They do not mean he is forced to close quickly. The difference matters. Trump can declare victory and walk away at any time. Iran does not have that option.

The US is the structural relative beneficiary of this crisis. Almost no one is discussing this. The US is the world’s largest oil producer at approximately 13.6 million barrels per day (source: EIA Short-Term Energy Outlook, March 2026 release). American energy self-sufficiency means the Hormuz closure is not an existential threat to the domestic economy. Every day the strait stays closed, Asian and European buyers are forced to redirect toward American crude. That market share shift, once it happens, is difficult to reverse. When Iran strikes Gulf neighbors’ infrastructure, post-war reconstruction contracts flow to American firms, security agreements flow to American defense contractors, and energy rerouting projects like the IMEC corridor are US-led. Trump handing the strait problem to Europe is not abandonment. It is calculated: the more desperate Europe gets, the more it needs Washington, and the stronger the American negotiating position becomes.

This does not mean the US bears no cost. Oil price increases are feeding domestic inflation. Military spending continues to climb. Alliance coordination burns political capital. The election cycle pressure is real. But relative to the cost Iran and the Gulf states are absorbing, the US sits at the structural advantage end. Trump is dictating conditions, not negotiating them.

Indifference is leverage. If Trump signals concern about midterm pressure, every opponent exploits it. Iran stalls for time. Europe waits for a rescue. Allies raise their price. By performing indifference, Trump forces every other actor to move first. The UK convened a 35-nation conference. Gulf states are building their own pipeline alternatives. According to the Associated Press, Pakistan has proactively offered to host US-Iran dialogue. Whoever cares less holds the stronger hand.

Infrastructure strikes are the highest-efficiency tool available. Maximum visual impact, maximum negotiating acceleration. A collapsing bridge on Truth Social accomplishes the military objective and the political narrative objective simultaneously.

Vance is optionality, not an escape hatch. Trump assigned the negotiation persona to Vance. My assessment: the structure gives Trump a victory claim regardless of outcome. A deal happens, it is Trump’s credit. Talks collapse, it is Vance’s problem. Walk away entirely, and the framing is mission accomplished. Trump is buying an option, not an exit.

April 6 is the next decision node. But for Trump, April 6 does not change the structural advantage. It only changes the timeline for harvesting it.

7. The Only Exit

Everyone is asking when the strait reopens and when the war ends. I am more focused on what comes after: who keeps Iran alive once the shooting stops.

Consider Iran’s strategic environment. The proxy network has disintegrated: Hezbollah decapitated, Assad fallen, Hamas functionally destroyed. Military capability is crippled. Nuclear facilities are destroyed. Supreme leadership has passed to a son with no independent authority. Overseas assets are frozen. And Israel is standing next to all of this, ready to launch another round at any time, without needing American permission.

Iran has three paths.

Path A: continued resistance. The outcome is slow death. No money, no military capability, no allies, Israel on standby, domestic unrest a matter of when rather than if.

Path B: lean on China and Russia. China will not fight for Iran. China buys discounted oil. Russia is consumed by its own problems. Economic partners, yes. Security guarantors, no.

Path C: align with the US in exchange for security guarantees. The price is abandoning the nuclear program, limiting the missile arsenal, restructuring the IRGC. The return is a security umbrella, sanctions relief, asset unfreezing, reconstruction assistance. Historical precedents with structural similarity exist: Libya’s 2003 nuclear abandonment, the post-war security arrangements for Japan and Germany. The Libya parallel carries an obvious caveat: Gaddafi abandoned his nuclear program in 2003 and was killed in 2011. The structural similarity lies in the transaction framework, not the outcome. Whether the outcome differs depends on whether the guarantor honors the guarantee. Japan and Germany suggest it can work when the guarantor has strategic reasons to sustain the arrangement. The parallel is in the deal structure, not the occupation model.

Path C is the best outcome for Iran as a country. It is a death sentence for the IRGC and the current ruling class.

Whether Iran should align with the US is almost beside the point. The harder question is who represents Iran at that table. According to public reporting, Pezeshkian has signaled willingness to engage in dialogue. IRGC hardliners’ public statements point toward continued resistance regardless of conditions. Trump’s reported 15-point plan may be a probe: which terms can the civilian government accept, which are the IRGC’s red lines, and who breaks ranks first.

Post-filing update (April 3): Former Foreign Minister Zarif published an article in Foreign Affairs calling on Tehran to “declare victory and end the war,” proposing a concrete framework for a US deal that includes nuclear program limitations, strait reopening, and comprehensive sanctions relief in exchange for a non-aggression pact (source: Foreign Affairs, April 3). This is the first time a member of Iran’s establishment has publicly articulated a face-saving exit path. Not surrender. “Peace after victory.” The pressure behind Path C is moving from backrooms to the public record.

Trump said “regime change has occurred.” Perhaps he was not describing the past. Perhaps he was describing what he expects to happen next.

8. Scenario Update: April 6 Is an Accelerator, Not an Escalation

My base case from Art. 16 holds at 60-65%, with a slight widening of the range.

The core assumption from the previous round was “infrastructure strikes extend the timeline.” That assumption needs revision. Striking the power grid does not push the war into a new escalation phase. It accelerates the collapse of Iran’s organizational capacity. The logic chain: power goes to zero, command and communications fragment, coordination required to maintain the strait blockade disintegrates, the IRGC degrades from organized resistance to sporadic harassment, Trump accumulates enough “we already won” material to declare mission accomplished by mid-April, and the strait question gets handed to a multilateral framework.

April 6 remains a binary event, but the nature has shifted from “escalation versus restraint” to “acceleration versus status quo.”

Base Case (approximately 60-65%)

Assumptions: April 6 strikes hit the power grid. Iran’s daily launch frequency continues declining. Civilian government or military pragmatists signal willingness to negotiate before mid-April.

Indicators to watch: daily launch count dropping to single digits; Pezeshkian’s public messaging diverging further from IRGC rhetoric; US strike tempo beginning to decrease.

Under these conditions, a mid-April exit window becomes significantly more probable.

Risk Case (approximately 25-30%)

Assumptions: April 6 hits the power grid, but Iran responds with actual strikes on Gulf state infrastructure (bridges, energy facilities, not just verbal threats). The war enters a bilateral infrastructure destruction phase. Exit window pushed to May or later.

Indicators: confirmed Iranian strikes on Gulf neighbors’ infrastructure (not threats); Brent sustained above $120; Gulf states publicly requesting additional US interceptor support.

This scenario requires reassessing energy exposure caps and recalibrating hedge strike prices.

Tail Case (approximately 5-10%)

Assumptions: American domestic opinion turns sharply due to civilian casualty footage. Congress initiates War Powers constraints. Or Iran lands a significant strike on a US military installation, triggering uncontrolled escalation.

Indicators: anti-war demonstrations reaching a scale Congress cannot ignore; Iran deploying remaining medium-range missiles in a concentrated salvo against US bases; Trump approval dropping below the 35% structural danger threshold.

This scenario invalidates the April 6 framework entirely and requires a full de-risking protocol.

Monitoring Dashboard

Assumption Invalidation Triggers

If Iran initiates formal negotiations through a verifiable channel before April 6, or if IRGC large-scale retaliation against regional infrastructure triggers a sharp reversal in American domestic opinion, the framework above requires recalibration.

9. What This Means for Allocators

For allocators, the core message from this analysis is straightforward: do not make large directional bets before April 6.

Path A: hold current exposure, wait for clarity. If you have already hedged and your position sizing is within tolerance, let the event resolve before adjusting. The cost is absorbing potentially severe volatility around April 6. This suits allocators with existing hedges and a quarterly-or-longer time horizon.

Path B: reduce exposure before April 6. Trim non-energy Middle East-related positions. Prepare dry powder. The cost is missing the rally if April 6 produces an unexpected de-escalation signal, though I assess that probability as low. This suits allocators with elevated exposure or low volatility tolerance.

Path C: use options to cap downside. Buy protective puts on Brent and correlated energy equities, preserving upside participation. The cost is time decay, and at current implied volatility levels, premiums are expensive. This suits allocators with derivatives capability.

Which path you choose is less important than knowing what you are giving up by choosing it.

Series Links

Art. 13 (Three-Layer Collapse): Established the IRGC internal fracture thesis that underpins the endgame analysis in this article.

Art. 13.5 (Post-Mortem): The principle that “multiple actors must be modeled independently” applies directly to the five-party dynamics in the Hormuz reopening framework.

Art. 14 (The Tollbooth): Introduced the Hormuz tollbooth. This article reveals the deeper motivation: desperation, not leverage.

Art. 15 (Managing the Coalition): Analyzed the multilateral framework for strait governance. The Infrastructure Trap is now eroding the conditions that framework depends on.

Art. 16 (Five-Tier Transit Rights): Base case maintained at 60-65%. April 6 repositioned from escalation node to acceleration node.

Positions should be sized for uncertainty, not for narrative confidence.

Disclaimer

This article reflects my personal investment philosophy. It is not investment advice. Make your own informed decisions.

Miyama Capital manages proprietary capital only and does not solicit external investors.

This memo represents the author’s personal views on macroeconomic conditions, interest rate environments, and asset allocation as of the date of writing. It does not constitute a solicitation, recommendation, or guarantee regarding the purchase or sale of any security, fund, bond, or other financial instrument. Investing involves risk; bond prices, interest rates, foreign exchange rates, and economic/policy conditions may materially affect asset values. Scenarios and instruments discussed may become inapplicable as market conditions change. Readers who make investment decisions based on this memo do so at their own risk, and the author accepts no liability for any gains or losses arising from the use or citation of this material.

Kuan H. Wang Founder & CIO, Miyama Capital