Greenland, Wall Street, and the Prisoner’s Dilemma: Why Proprietary Capital Has an Edge

How agency risk and mandates create temporary mispricing—and how proprietary capital can exploit time arbitrage.

Executive Summary

The Diagnosis: This wave of “synchronized stress” resembles a liquidity shock driven by narrative rather than permanent fundamental impairment.

The Reality: A full-scale “territorial annexation” scenario is practically infeasible under U.S. domestic and institutional constraints. The realistic path is incremental escalation: mission upgrades and infrastructure expansion used as recurring bargaining chips.

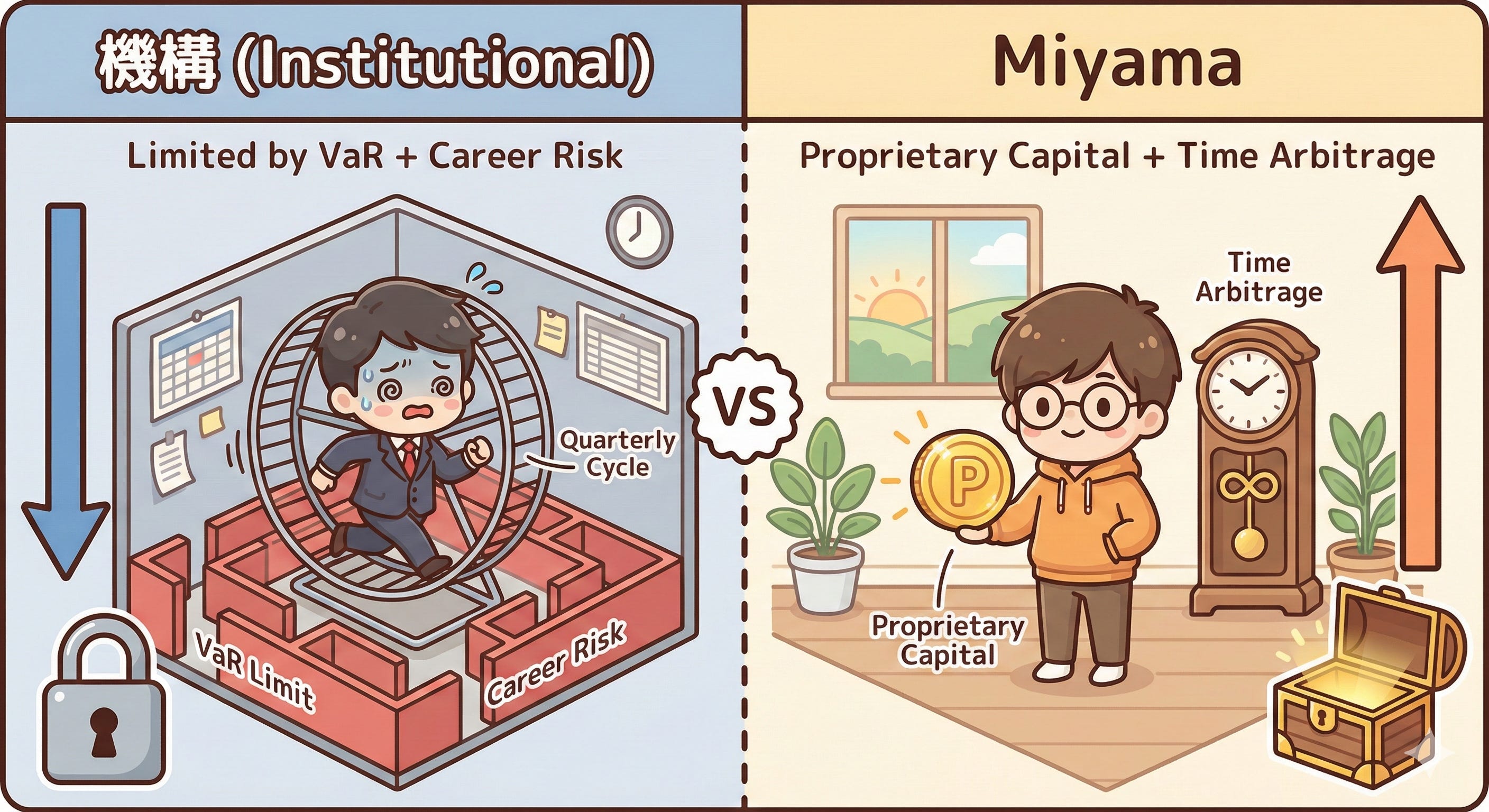

The Mechanism: Institutions cannot set tail risk probabilities to zero. To prioritize career survivability, they must deleverage liquid core assets.

The Opportunity: This creates a window for Time Arbitrage. The goal is to accept controlled volatility in exchange for mean reversion.

Over the past 72 hours, global markets have exhibited a classic pattern of synchronized stress: risk assets sold off, yields spiked, and the dollar weakened.

I view this not as a fundamental inflection point, but as geopolitical narrative amplification colliding with mechanical institutional deleveraging. This setup invariably creates short-term pricing dislocations.

A recurring question I hear is: “If the consensus view is that the Greenland conflict is largely political theater, why is Wall Street forced to sell?”

The answer is blunt. Institutions do not have the mandate to take binary directional bets. They are trapped in a structural game defined by Agency Risk. Career risk, compliance strictures, and VaR constraints compel them to sell at precisely the wrong time.

This note applies first-principles reasoning to map the logic behind the sell-off and explains why proprietary capital is uniquely positioned to harvest the resulting time-based edge.

1. Macro Lens: A Conflict “Priced In” but Politically Hard to Execute

Let’s strip away the emotion and isolate the variable triggering the panic: Greenland.

Current market pricing seems to embed an extreme tail event: a U.S. military seizure of Greenland that fractures NATO. However, decomposing this scenario reveals its improbability.

The “Boots on the Ground” Reality The U.S. already operates the Pituffik Space Base (formerly Thule) in Greenland. This is the U.S. military’s northernmost installation and a critical node in the ballistic missile early warning system.

If the strategic objective is a “stronger Arctic presence,” invasion is redundant. The U.S. is already on the island. The logical path is simply to operate within existing frameworks to upgrade missions and infrastructure.

The Real Algorithm: Leverage, Not War I model the current administration’s posture not as military mobilization, but as leverage. The strategy links NATO commitments to trade instruments (tariffs) to force European defense spending. This is a reusable negotiation tactic, not a war plan.

Markets are mispricing a negotiation tactic as an existential conflict.

2. The Institutional Prisoner’s Dilemma

If the war script is infeasible, why are multi-billion-dollar managers selling?

Tail Risk Asymmetry Since the administration change, markets face a structural problem. The probability of tail risk cannot be marked to “0” in risk models. The payoff function is asymmetrical for a fund manager:

Buy the dip (Scenario: Bluff): You earn a few points of alpha. Good, but not career-defining.

Hold and fail (Scenario: Black Swan): If risks materialize, the drawdown is existential. You risk being fired or redeemed.

Inside a VaR framework, the only “approved” response to low-probability/high-severity scenarios is to cut exposure.

Agency Risk As Keynes noted, it is better for reputation to fail conventionally than to succeed unconventionally.

When the herd sells, selling is “prudent risk management.” Holding is “reckless.” Managers optimize for career survivability, not absolute truth. This is Agency Risk, not a lack of market IQ. They are forced to sell.

3. The Hunting Ground for Time Arbitrage

When drawdowns are driven by model-driven deleveraging, the assets being sold are often the most liquid core holdings (Big Tech, Quality Growth). They are sold not because they are bad assets, but because they are the easiest ATM to access.

This is where Proprietary Capital has the edge.

Unlike institutional managers, we are not constrained by monthly reporting, external redemptions, or the optics of short-term volatility. We possess the scarce resource of Time.

The Strategy

Our Edge: We do not need to justify NAV swings to LPs. We do not need to make consensus-friendly decisions at peak fear.

The Trade: We buy the liquidity proxies that institutions are puking out. We are effectively selling them the “certainty” they crave and buying the “volatility” they fear.

The Discipline: Leverage control is non-negotiable. We must ensure we are never forced out of a position before the valuation repair arrives.

Conclusion

This is an asymmetrical battle.

On one side, you have institutional giants handcuffed by models and career risk. On the other, you have independent capital capable of holding through the noise.

When the market crashes because of a “zero-probability” war, I don’t see fear. I see a historical transfer of wealth from those who are forced to sell to those who are free to buy.

Disclaimer

This memo is for educational discussion and internal-style research notes. It is not investment, legal, or tax advice. Rules and tax regimes change, and outcomes depend on individual facts and jurisdiction. Consult qualified professionals before implementing leverage or tax planning.

Kuan, Founder of Miyama Capital